Q3 2024 Letter to Investors

Please View the Disclaimer at the Bottom of the Post

To view the pdf version of this post, please check out our investor materials page our go to the invest page on our website. If you are an interested accredited investor please view our invest page for our marketing materials and reach out to us via our contact page.

Q3 2024 Letter to Investors - October 20th, 2024

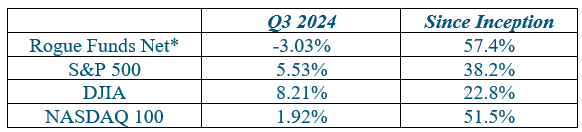

During the third quarter of 2024, Rogue Funds LLC (the “Fund”) appreciated -3.03% net of fees*. As I predicted in our last quarterly letter, volatility increased significantly but obviously not in our favor. Due to the Fund’s concentration, it will not be unusual to see both large drawbacks and large increases in the overall returns seen throughout the year, but I will do my best to minimize this and I am disappointed in some of the positions from this quarter.

Our portfolio turnover picked up slightly considering the first time we lost, what I feel is more than just normal volatility, but permanent capital loss. This is unacceptable and something I strive to minimize. With our newfound cash we have added 2 new core holdings that I have intense conviction in. Most of the companies in our portfolio will experience strong catalysts over the next 12-15 months that I believe will allow us to experience a fairly market neutral increase in the portfolio’s value.

Seed Fee Structure

Currently, the Fund is offering a seed fee structure utilizing a 10% incentive allocation (compared to a 20% incentive allocation once the seed round ends). We are now only offering the start-up fee structure to individuals investing $500,000 or more for the foreseeable future. All investors who participate in the seed funding are locked into this structure for the entirety of the time that they choose to stay invested in the Fund, including any additional capital.

Performance and Returns

*Unaudited Net Return Data for the Rogue Funds, LLC Portfolio, net of all fees and expenses and 20% incentive allocation.

I poorly predicted last quarter that our portfolio would only experience an increase in turnover if we were to experience unexpected increases, but instead we experienced two positions that lost a substantial amount of value in a fairly short period of time. I will go into detail on these positions and what happened later in the later. Looking forward, I am extremely confident in the rest of our portfolio’s ability to appreciate substantially over the next 12 months and I will explain both our new positions and the future expectations of the portfolio.

*Unaudited Net Return Data for the Rogue Funds, LLC Portfolio, net of all fees and expenses and 20% incentive allocation (from May 1, 2023, to September 30, 2024).

Summary of the Fund Performance

We experienced a minor dip in the value of the portfolio which I am significantly disappointed by. We had two core positions decline by 50%+ in the period since we have owned them which was due to substantial changes in their investment theses. We have since sold out of those positions which I discuss further in depth below.

As management for each position executes (or fails to execute) their strategies I will keep you updated through both our quarterly letters and the blog which can be found at www.rogue-funds.com/blog.

Mistakes

Swedish Stocks led the way in poor performance for the portfolio and I will talk about our two losers below:

Moberg Pharma

{Redacted for Limited Partners Only}

Checkin.com Group

This was a position that we have owned for a very short period of time. It is a biometric check-in company. I was under the impression that they had scored very large contracts with both Klarna and Ryan’s Air and they were scaling their technology into those two companies. It turns out after a public press release that they were lying about scaling into Klarna. Honestly the company was never cheap, but I believe it had decent operating margins and could scale. This was completely my fault in paying too much for a company, leading to an increase in risk. I don’t think there is a redeeming situation for us here and management lying put a bad taste in my mouth. We have sold this position for significant losses. This was a hard lesson in ensuring that I uphold extremely high valuation standards for our portfolio to ensure protected downside.

Core Holdings Breakdown

I will breakdown the performance of the Fund in order of current holdings/recent divestments then I will break down new long-term additions to the portfolio. I will provide significant updates from the quarterly reports for each position. At the beginning of each investment update, I will link you to our initial investment thesis for that position which can be found on our blog.

ASP Isotopes

I have contacted you all individually regarding this investment and we had significant news hit the portfolio last week. This has allowed the price to skyrocket on confirmation of the Quantum Enrichment technology at commercial scale. They have numerous catalysts (I think 8 major catalysts) expected to hit in the next 6-8 months. I think with so much short interest we still have a long way to go. We’ll continue to monitor this position going forward. This is our largest position in the portfolio by a substantial margin.

ElectroCore

We added ElectroCore about ~1.5-2 months ago and we are very excited about this high growth and high margin business. Management is excited about it as well and showed it by buying $6m of their last $8m raise. They hit profitability in about 6-9 months while growing revenue at a 70% consistent CAGR and new devices beginning to scale. I will be releasing a full DD breakdown on this one in the coming days. It is now our second largest position.

HAYPP Group

We wrote about HAYPP group on the Rogue Funds blog and highly advise you to check out the full post. HAYPP is a Swedish online retailer of nicotine pouches and has the market leading position among e-retailers. Currently their profitability is hidden by their growth in new markets such as the US, UK and other large markets. Their operating leverage will have them taking their EBITDA margins from -2% to 8% by early to mid-2025 (with little capex). Their growth in the US has been at a huge 40%+ y/y rate that I believe could be even higher currently. Based on online monitoring, their sales are climbing at unprecedented levels, especially as competitors take market share away from the leading nicotine pouch manufacturer, Zyn. A larger breakup in the branding of nicotine pouches benefits HAYPP as customers seek out variety by going to non-brand specific retailers.

They are undergoing some selling pressure due to increased regulations on their snus business which might impact the topline in the back half of this year but that was getting rapidly cannibalized by their nicotine pouch business anyways. The biggest impact is the regulations in California for selling flavored nicotine pouches, that will be interesting to see, and it could lead to a large (but temporary) impact. This is the 3rd largest position in the Fund.

Global Atomic (Uranium)

We finally bought some more Global Atomic for the first time in a while. We continue to walk against the crowd despite the risk which we believe will continue to mitigate significantly. Let’s take another look at our risk breakdown below:

- Niger gave Global Atomic an official letter of approval. This is a huge deal and will help considerably with the development bank granting a loan.

- Their financing is a huge risk due to the perceived geopolitical risk and if they get good terms this will serve as a serious catalyst for the company. Bad financing terms are already relatively priced in as most experts expect poor financing terms and the stock remains near 4-year lows. The company will produce $200m in FCF when the mine is in full production, which is well more than the current price of the stock.

- The company announced that they should hear from the credit committee from the development bank in October (this month).

- Despite headline news articles, there are still no signs that Russia has taken any specific interest in any of the mining rights of any mine and there is very little sign of cooperation with Russia in general. Niger seems to be pushing back against most large global influences.

- The IMF has restarted their payments to Niger showing international cooperation.

- If Uranium prices move back above $100/lb, which seems very likely, then this has the potential of 5x-10x depending on how high prices move. If uranium merely maintains their current position, then I believe we could see a 3 – 5x in the position.

- Zinc prices have continued to move up which could make their Zinc facility a boon to the balance sheet to raise cash.

- The CEO of Global Atomics has a major position and hasn’t sold.

- History of minimal dilution for a mining company.

- The company will need to dilute slightly further to capture the rest of the needed capex for the mine but at that point the stock price should (hopefully) be re-rated due to a deal from the development bank.

We believe that the price is poorly reflective of the true risk the company has. I think there is a very high chance we see a double or triple in the stock within 6-12 months depending on uranium prices and financing. Once pounds start being produced most risk will be taken off the table and we will continue to collect the returns of this perceived risk. Uranium is still in a deficit so prices should maintain a high level for the foreseeable future. With recent price appreciation and our lower DCA this is now the 4th largest position in the fund.

Aware

You can read more about this investment on the Rogue Funds blog here. As I explained in my initial report, Aware is a lumpy revenue business (converting to a smoother long term ARR business) and this continued in the Q2 report. Q2 looked fairly good but the stock has since declined back to the pre-quarter release levels due to the fact that the market does not think they are in a place to grow at 15% above their Q3 standards from last year (which was a blockbuster quarter). The good news is that the management team is firing on all cylinders when it comes to the cost-cutting strategy, which is directly in line with management expectations. The bad news is that they no longer have their chief revenue officer. They are now getting into the check-in biometrics business which is growing very rapidly but has a lot of competition. The downside is very limited with Aware ($29m in cash and $40m market cap) as it is very unlikely that they will ever trade below cash since they are sitting very close to breakeven (stopping cash burn). We did take some profits (but not much) off the table here and it is the 5th largest position in the fund.

RADCOM, Inc (Unchanged since last letter)

Radcom is an Israeli 5G assurance company that I have been monitoring for a couple quarters as they inflect profitably. Because their biggest owner died and their CEO resigned (he still works with the company in an advisory role), I was curious how this would impact the company as they entered a very high marketing phase. After putting a lot of R&D into the company’s technology they are beginning to put those costs into marketing to grow the business in areas like Asia and Europe. This has been working even better than expected as they have already entered into multi-year agreements with huge 5G companies. Their growth has been much better than expected and the sales team is firing on all cylinders. They have a boatload of cash that they plan on using to acquire a company that meets their standards. The current management and board have not been able to identify any quality acquisitions, and I would not be surprised to see them begin to buy back a substantial number of shares. The best part about this investment is that as they continue to execute above expectations, their stock price has continued to go down and made a great buying opportunity for us. I will be posting an article regarding Radcom soon that will go more in depth into this position. This is the Funds 6th largest Position

Abaxx

Abaxx is a small exchange based out of Singapore. It is ran by veterans from Goldman Sachs, NYMEX, CME, and SGX. Insiders own a decent amount of the stock. They are beginning to grow and would like to be profitable. I believe that even if they are not able to break even that the company will be able to sell off its various assets for more than the stock price. I think there is a lot of momentum here and they have a near monopoly in some of the smaller markets they have created without much chance of larger exchanges get involved. I think this one could prove to have huge potential. It is the 7th largest position in the Fund, and we will share more details in the future on this position.

Mitchell Services (unchanged from last letter)

You can read more about this investment on the Rogue Funds blog here. Their stock price has appreciated about 20% from when we first took our initial position. Mitchell Services is a drilling services company based out of Australia that took advantage of the instant write-off program that ended in 2023. This allowed for rapid growth while also hiding earnings (but pushing FCF) as depreciation remains near highs. As the earnings begin to increase, the company is much more likely to be noticed just as they enter a return to shareholder strategy that is being pushed by their chairman and largest shareholder. Currently they have a 10% buyback program in place and a 5% dividend. I believe they have a possible 4-5 bagger potential based on the current share price. This is the 8th largest position in the Fund.

Achieve Life Sciences, Inc (Stock and Calls)

You can read more about this investment on the Rogue Funds blog here. The company will release results in Q1 at which point I think we will see a minor run-up before release and then a major run-up after this release. This will cause a massive re-rating in the stock in a very short time period. In the meantime, we have a rolling calls position that will continue to drain the portfolio for the next 6-9 months. We should see an NDA in 2Q 2025 and then PDUFA around Q4 at which point they will probably already be bought out. This is the 9th largest position in the Fund.

Advanced Micro Devices, Inc. (AMD) Puts (Sold Out)

We sold our AMD puts for a sold profit after the Japan Carry Trade caused volatility to spike considerably and allowed for a significant increase in the value of our put options. I felt that was an ideal time to capture these profits which has turned out to be a good choice in hindsight.

Structure, Fees, Expenses, and Performance Allocation

I have stated in each letter that the Fund will continue to experience volatility that most investors are not comfortable with or are not used to. In this quarter alone, we had substantial changes in the valuation of the Fund within any given month. Investors of course view a relatively “smoothed” version of this volatility but there is a real chance that unlucky timing could result in our monthly performance or quarterly performance being severely impacted by these short-term swings.

Because of this, it is in each of your best interests to carry a long-term oriented view of the Fund’s performance. I will continue to reiterate this quarter to quarter and year to year. We are looking for investors who share this ideology and are willing to bear with us through periods of short-term volatility. Many investors throughout history have panicked during moments of heightened volatility and it has cost them greatly to do so. We wish to avoid this for both the Fund’s benefit and each of our investors’ benefit. Each of our investors thus far has held onto their long-term orientation and it has benefited everyone. I appreciate each of you for your endurance as an investor in the Fund and I am extremely proud to have you as a Rogue Funds investor.

Tax Commentary

Our goal is to hold positions for over a year (and even longer for quality compounders) to encourage long term capital gains benefits but, if I feel that it is in the long-term benefit of investors to sell early, then I will sell early.

Frustratingly we still experience a lot of turnover, but this time it is due to a loss of permanent capital. This will be enough to offset any capital gains we should experience this year (barring extreme changes in core holdings in the next few months). In hindsight I should have held Sezzle longer than what I did to capture both a higher share price and a conversion to long term capital gains. I don’t think I made a horrible choice, but I believe Sezzle is getting into overvalued territory and has maintained extreme volatility (insiders continue to sell heavily as well). Sometimes that is the luck of the draw, and I felt it was in our best interest to capture our gains.

Looking back at each position that we have sold, it has easily been in the Funds best interest months later to have sold most of those positions when we did outside of Sezzle and I will try to continue to reduce your tax burden without substantially hurting returns of the Fund. As I monitor our past core positions, I will ensure I identify times when I sold too early that led to a significant tax burden on investors and try to correct those issues in the future.

Retirement accounts are currently able to invest in the Fund, please contact me if you would like to invest via an IRA as there are certain limitations in the amount you can invest.

Structure and Fees

As many of you are aware, the investors in the Fund bear few costs aside from the management fee and the incentive allocation. The management company covers most expenses creating an extremely friendly expense ratio for all our investors. The management company is funded by equity from myself and the one percent management fee which is extremely sustainable and investor friendly to try to keep the expense burden off investors. Initial investor minimum allocations are still $100,000 with additional subscriptions of $25,000.

Update Schedule

I will continue to update each of you through our quarterly letters and you can view our updated tear sheet on the website each month. These updates will usually occur sometime between the 15th-25th of each month.

For the first three quarters of each year the letters will be shorter, mainly contributing to a summary of performance for that quarter and any substantial changes in either the portfolio or the structure. The 4th quarter of each year will continue to be our most substantial letter.

Summary

I would like to thank each of you for investing in Rogue Funds, LLC. If you have any questions, please email or text me as needed. I will continue to look forward to the future years running this Fund. As always, I would also like to thank my beautiful Fiancée for editing this letter while also being my biggest supporter and the best partner I could ask for.

Respectfully,

Jacob Rowe

Chief Investment Officer

Rogue Funds, LLC

Disclaimer

This document is being provided to you on a confidential basis. Accordingly, this document may not be reproduced in whole or part, and may not be delivered to any person without the consent of Rogue Funds Management, LLC (the “Manager”). Nothing set forth herein shall constitute an offer to sell any securities or constitute a solicitation of an offer to purchase any securities. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents for Rogue Funds, LLC, managed by the Manager, which include, among others, a confidential offering memorandum, operating agreement and subscription agreement, as applicable. Such formal offering documents contain additional information not set forth herein, including information regarding certain risks of investing in a Fund, which are material to any decision to invest in a Fund.

No information in this document is warranted by the Manager or its affiliates or subsidiaries as to completeness or accuracy, express or implied, and is subject to change without notice. No party has an obligation to update any of the statements, including forward-looking statements, in this document. This document should be considered current only as of the date of publication without regard to the date on which you may receive or access the information.

This document may contain opinions, estimates, and forward-looking statements, including observations about markets, industries, and regulatory trends as of the original date of this document which constitute opinions of the Manager. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Actual results could differ materially from those in the forward-looking statements due to implementation lag, other timing factors, portfolio management decision-making, economic or market conditions or other unanticipated factors, including those beyond the Manager’s control. Statements made herein that are not attributed to a third-party source reflect the views and opinions of the Manager. Opinions, estimates, and forward-looking statements in this document constitute the Manager’s judgment. The Manager maintains the right to delete or modify information without prior notice. Investors are cautioned not to place undue reliance on such statements.

Certain information contained herein has been obtained from third-party sources. Although the Manager believes the information from such sources to be reliable, the Manager makes no representation as to its accuracy or completeness. Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Targeted returns reflect subjective determinations by the Manager based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Unaudited net return data for the Fund is estimated, net of all fees and expenses (From inception on May, 2023 through March 31, 2024). The net return presented is also net of Incentive allocation of 20% unless stated otherwise.

The past performance of the Fund is not indicative of future returns. The performance reflected herein and the performance for any given investor may differ due to various factors including, without limitation, the timing of subscriptions and withdrawals, applicable management fees and incentive allocations, and the investor’s ability to participate in new issues.

There is no guarantee that the Manager will be successful in achieving the Funds’ investment objectives. An investment in a Fund contains risks, including the risk of complete loss.

The investments discussed herein are not meant to be indicative or reflective of the portfolio of the Fund. Rather, such examples are meant to exemplify the Manager’s analysis for the Fund and the execution of the Fund’s investment strategy. While these examples may reflect successful trading, not all trades are successful and profitable. As such, the examples contained herein should not be viewed as representative of all trades made.