Mitchell Services is a Potential 4-Bagger Hidden by a Tax Write-off Scheme

Due to my audience having few Australians and both currencies’ being relatively stable, I will be referencing all financials in USD rather than AUD with AUD numbers in parentheses.

Mitchell Services ($MSV.AX)

Do you know the saying about “During the gold rush, sell shovels.” What this saying is referring to is you don’t want to be the person trying to dig for gold since there is a ton of risk and the odds of striking it rich are slim. So, instead of being the person finding gold, you should be the person who sells the shovel since as long as people continue to look for gold you will make money without the risk of being a gold digger. This exact situation pertains to Mitchell Services (MSV.AX).

MSV (an Australian company) sells drilling services to mining companies Over 90% of their customers are global mining major companies (for those who are unaware, majors in general tend to contain much less inherent risk than junior miners leaving them with recurring customers). Their revenue is split 55% towards surface drilling and 45% for underground drilling.

They do have some risk with ~40% of revenue coming from gold services and 40% coming from coking coal services (although it should be noted that they have no exposure to lithium or nickel). Gold has reduced its share as a part of the commodity mix with coal and lead/zinc/silver increasing significantly. This change can be seen in the diagram below. This swing in commodity exposure illustrates how important it is that the company sells drills to a mix of commodities, hence reducing its overall risk as demand switches from one commodity to another.

Earnings Hidden Through Instant Write Off Scheme

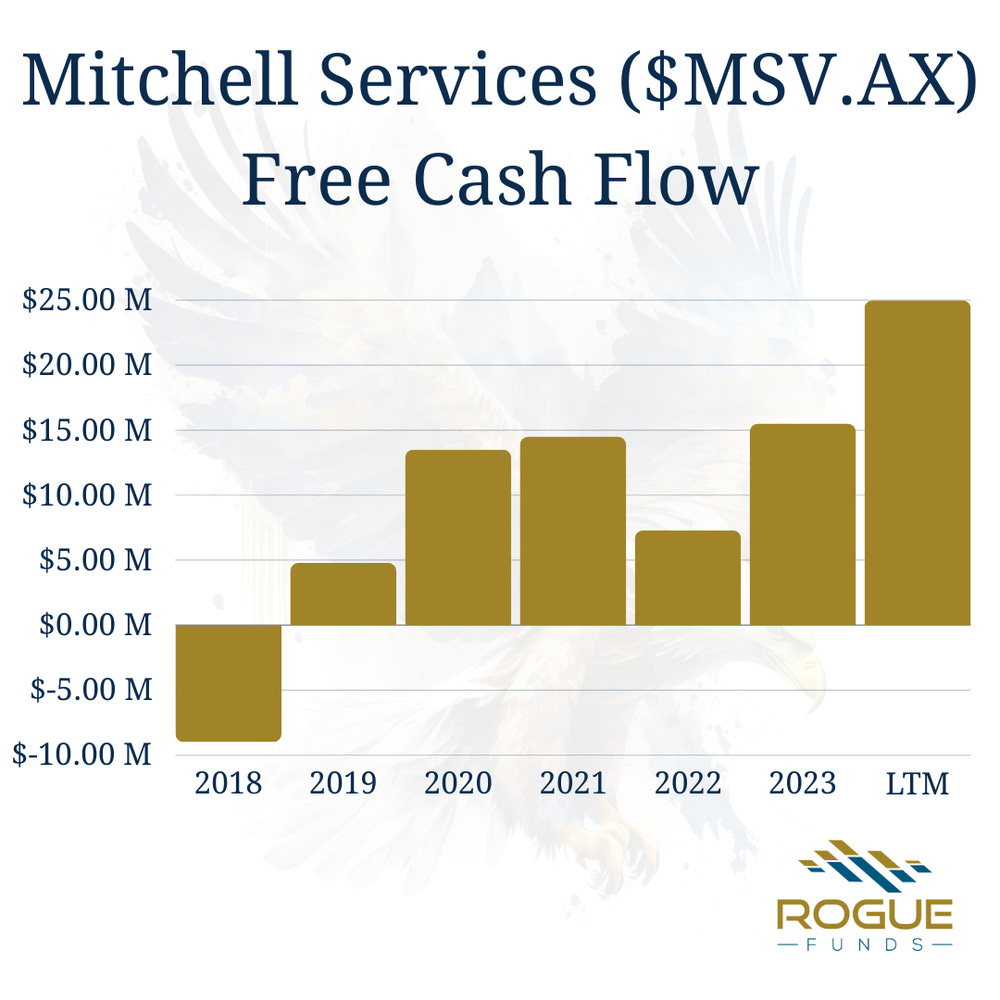

Mitchell Services has been a continuously growing company from a revenue standpoint for almost 5 years, even as its stock price has slowly worked its way down. The driving force behind the lagging stock price is that earnings have not grown on the same path as revenue.

But if we look at Free Cash Flow (FCF), we get a completely different story where they have produced nearly 50% of their market cap, at least, in FCF for the last 3-5 years with the last 3 years experiencing a doubling in free cash flow.

So, what is going on with this disparity? Let’s introduce the instant asset write-off program that was create by the Australian taxation office. This program was introduced in 2020 and allows companies to instantly write off assets (as the name implies). The consequences of this are hampered operating income, lower taxes, and an increase in Free Cash Flow. The below chart signifies the massive increase in Depreciation and Amortization (D&A) that began in 2020.

This program will benefit them for the next 2 years until late 2025/2026, in which case they will pay zero income tax over that timeframe. Of course, after the program ends it can be assumed the D&A will be lower than pre-2020 levels which as bad as that sounds just doesn’t matter because the company has been writing off ~$18m USD ($26m AUD) a year for the last 3 years and will continue to do so for the next 2 years. We’d much rather have this cash today and avoid paying taxes today, so this is extremely beneficial to the long-term outlook of the company. Although this is extremely beneficial to the company for the long term, it hampers earnings then combined with it being listed on the Australian Stock Exchange, it only having a small market cap, and the growth of shares outstanding while revenue increased (20% total growth in share outstanding since 2018, with a -6%+ change in shares outstanding since 2021), it has caused this company to be heavily overlooked.

Outlook Going Forward

The company continues to fire on all cylinders, and it seems that will continue with their Net Profit After Tax (NPAT) expected to break their 2023 record along with the surface fleet basically being completely booked out. Their working capital continues to thin down which also has led to major increases in cash flow. $4.6m ($7.1m AUD) in additional cash flow has been added in just 1H 2024 due to tighter working capital.

I don’t expect revenue to continue at the breakneck 30% pace which was mostly due to accretive debt uptake to increase their drill rigs when interest rates plummeted in 2020 but it should be noted that they have been able to double revenue since 2019.

I still expect revenue to increase as commodity demand stays elevated although they did report that they are seeing that exploration has weakened which is a risk to note. Management reported that they are no longer focused on topline growth as much and plan on returning cash to shareholders after their multi-year growth plan hits its end. Their main goal now is to reward shareholders for the growth the company has experienced.

They do have some routes of increasing top-line by increasing their underground rate (which management is fairly happy with current usage rates), increasing drills which has been indicated around 2 drills added per year, or expanding into new commodities which management is always looking to enter. Overall, I wouldn't expect revenue growth to be much more than 3%-5% for the next couple of years while management focuses on returning cash to shareholders.

Capital Allocation Strategy

Currently management is focused on following through with their commitment of returning cash to shareholders. Since the beginning of 2023 they have returned $8.6m ($13.2m AUD) to shareholders (not including the most recent dividend). Management doesn’t intend on growing (top-line) significantly until they see better opportunities. Currently they are intending to return cash to shareholders after investing in the growth of the business significantly over the past 3-5 years and that is their focus going forward.

Previously management needed an average of ~$8m ($12m AUD) in maintenance capex and they tended to continue to grow through growth capex of $10m ($15m AUD) which has led to consistent revenue growth as they increased their drills. Last year the company cut maintenance even further below that $8m maint. capex average to $7m ($10.5 AUD) leading to gushing free cash flow of $27m ($50m AUD) or 50% of the enterprise value of the business. They expect the maintenance capex to continue to trend closer to $4m along with cutting growth capex (except where they identify very good deals) while they focus on their new return to shareholders strategy.

The current strategy is to deliver 75% of NPAT to shareholders via dividend (~12% dividend) due to a prior commitment that they made for this year, and they want to see that strategy through. They have also been buying back shares but are down to a couple of thousand dollars left in their plan to buy back 10% of shares. Management seemed very open on the call for a switch from dividends to share buybacks in the future (the Chairman of the board was on the call), and it is something to watch.

The Board will continue to try to increase the share price, as over 30% of the company is owned by 2 individuals on the board and 20% is owned by the founder/chairman, Nathan Mitchell. Nathan seems to have a fairly active role for a chairman as he was answering questions on the conference call and is well aware of the different strategies to implement to increase their stock price and get investors to notice them (which is why they wanted to stick to the dividend to prove they will practice what they preach). I expect management to continue to cater to ways to lift the stock price while they search for opportunities.

Valuation

Right now, management is happy sitting in a low growth stage while biding their time and they are sitting at roughly 50% FCF yield which is simply insane. A dividend of 12% is great for shareholders while we wait for the market to recognize the potential in this company.

At this point it is obvious that management is extremely opportunistic and has a strong capability to grow the company when the opportunity arises. I don’t know how long they will sit in the return to shareholder mode, but I wouldn’t imagine it will be more than 3-5 years before management starts trying to grow the company again. I would think that 5%-8% top-line growth seems very feasible for the next decade but again that’s merely a guess.

To be safe we’ll assume an 8x multiple of FCF due to possible lumpiness in the business and assume low growth. If they achieve their goal of $4m maint capex this leaves us with about $30m in FCF. This gives a valuation of roughly $240m or 4.2x their current enterprise value. In comparison to the stock price of $.365 AUD/share this implies a valuation of $1.45 AUD/share. Obviously, I have left a ton of upside on the table in this valuation, and it just goes to show how insane this valuation is.

Conclusion

It is definitely in the shareholders’ best interest for management to buy the stock back as much as possible at these prices with the stock price trading at nearly 25% of intrinsic value and hopefully they switch from their current dividend track to a share buyback track. Management has been fantastic in their ability to execute over and over again and I expect that to continue through their return to shareholder plan.

Disclaimer: The author of this idea has a position in securities discussed at the time of posting and may trade in and out of this position without informing the reader.

Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

This article may contain certain opinions and “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential,” “outlook,” “forecast,” “plan” and other similar terms. All such opinions and forward-looking statements are conditional and are subject to various factors, including, without limitation, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors, any or all of which could cause actual results to differ materially from projected results.

Join the Rogue Funds, LLC Newsletter

Get portfolio updates, stock analysis, quarterly letters, and other hedge fund updates!

Email Address Subscribe

We respect your privacy.

Thank you!

Hi Jacob,

fellow $MSV shareholder here. What were your thoughts on the FY 2024 results? It did strike me that maintenance capex ended up much higher than hoped and capex guide for next year as well...

Interesting idea - certainly looks cheap.

How is maintenance capex defined by management? The definition investors should use is the level required to maintain both competitive position and unit volumes. However, I think some managements use it to mean literally the capex they spend on equipment maintenance. Obviously, drills have a finite lifetime, so as well as the cost of keeping existing ones in good nick, it should also cover the cost of replacing the fleet as they expire. I'm just a little skeptical about maintenance capex being $4m when D&A is $18m.

Also, a little confused about the write-off programme. I get investments being immediately written down to reduce taxable income - are the investments also depreciated immediately (or over the course of a year) to 0 in the income statement?