ASP Isotopes: Capitalizing on Semiconductor Trends, Nuclear Trends, and Deglobalization

Our Fund has a position in securities discussed. Please view the disclaimer at the bottom of the post.

ASP Isotopes

ASP Isotopes is one of the most unique companies I have ever come across. This is not a company that will screen which I believe has contributed to its current market value along with heavy dilution, but it presents an opportunity that I believe is very rare for investors and could present an opportunity for a 100 bagger if management is able to execute over the next decade.

What does the company do?

The company is at its core an isotopic enrichment company. Isotopic enrichment is not as complicated as it sounds. I’ll explain the science below.

First, what is an Isotope?

An isotope just refers to an atom's specific atomic weight. This is because atoms can have different atomic weights with different properties based on the number of neutrons they contain. Sometimes additional neutrons can be found (such as Carbon-14) or neutrons can be missing (such as Plutonium-239) and sometimes they’re isotopes found on the periodic table (Carbon-12 and Plutonium-244).

So, what is enrichment?

Let’s take Carbon for example. Carbon has 6 protons, 6 neutrons, and an atomic weight of 12 (remember protons plus neutrons equals your atomic weight), which we’ll call Carbon-12. Roughly 98.9% of all carbon found on earth is Carbon-12, about 1.1% is Carbon-13 (7 neutrons), and roughly 1 in 1 trillion carbon atoms are Carbon-14. If I were to enrich Carbon-14 that merely means I will increase its presence as a percentage of the total molecule. So, instead of Carbon-14 being 1 in 1 trillion atoms in a molecule, I will “enrich” it to 85% of the molecule so that it can be used in medical lab tracing.

The reason for enrichment is because Isotopes can produce unique properties such as radioactive decay or they can be unstable in comparison to their stable counterparts. For example, Carbon-14 is radioactive via beta decay (beta decay is a process where a neutron eventually transforms into a proton) which is relatively harmless to the body with a half-life of 5,730 years (the half-life means that roughly half of the Carbon-14 molecule will have turned into Nitrogen-14 at the 5,730 year point). Due to the long half-life and harmlessness to human health it is great for dating (carbon dating) and medical lab tracing so that scientists can see how a drug spreads in the human body. Enriching allows a higher percentage of an isotope in a molecule for scientists to utilize.

Traditional Methods of Enrichment (Explained Simply)

Currently the main method of enrichment for most molecules is gas centrifuge. But I’ll go through the main methods below in very simplistic terms so that each of you can understand:

Diffusion

Two isotopes with the same energy will travel at different velocities. Obviously, these different velocities are ludicrously small, and it takes many stages to actually get to a desired enrichment leading to high energy usage and costs.

Centrifuge

Almost all current commercial enrichment facilities on earth are centrifugal. At a very fundamental level imagine a large centrifuge spinning very fast with a molecule sitting in the center. The heavier isotopes in the centrifuge will slowly be forced to the outside of the centrifuge via centripetal force. Centrifuges are limited in size so they are basically split into numerous small centrifuges that cascade with lighter isotopes going to one centrifuge and heavier isotopes going to another centrifuge.

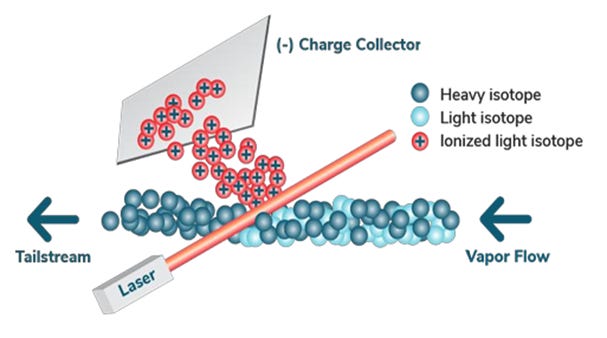

Laser

Laser seems to be the most accurate and energy efficient way of enriching, usually with an aim towards atomically heavier elements. Building the facilities and “know-how” is very expensive and I don’t believe there are any laser enrichment facilities for commercial production. Most are in early research phases. Laser enrichment basically ionizes (or gives a charge) to target isotopes which are identified by how light/photons interact with each isotope. Once they have ionized the desired isotope, they add an electric field which removes the isotope. Most laser enrichments are associated with uranium enrichment. Major *future* competitors of note will be focused on some variety of this technology. The two most common forms of enrichment are Atomic Vapor Laser Isotope Separation (AVLIS) and Molecular Laser Isotope Separation (MLIS).

More info on AVLIS and MLIS: https://www.nrc.gov/docs/ML1204/ML12045A051.pdf

Company History

ASPI was founded by Paul E. Mann (CEO) and Robert Ainscow (COO) in 2021. Mann was originally a research scientist at Procter and Gamble turned biotech analyst and Ainscow worked in investment banking. Roughly around 2020, a company called Klydon was in financial distress and reached out to Ainscow to restructure their debt. Klydon was run by a small group of nuclear physicists who had produced their Aerodynamic Separation Process after working in the South Africa nuclear field in the 80s and finally had the technology to accomplish the method. Like many individuals have seen with geologists in the mining industry or scientists in the pharma industry, they were not the best capital allocators. Their debt was not able to be restructured and the company had to file for bankruptcy in 2021.

Ainscow contacted Mann that Klydon was a “gold mine” and that they should buy the company out, so they worked on obtaining the needed nuclear licenses in South Africa before Klydon’s assets were put up for auction. Mann and Ainscow were the only bidders due to having the appropriate licenses and bought the assets for $750k with a rough estimated actual value of $15m+.

PLEASE TAKE ONE SECOND TO LIKE THIS POST

ASPI retained the entire Klydon team including the current Chief Technology Officer, which was the prior Klydon CEO and Klydons Chairman who is now the chief scientific advisor for ASPI.

Both the CEO (Dr. Strydom) and Chairman (Dr. Ronander) of Klydon has helped pioneer the field of AVLIS and MLIS study. Dr. Ronander is one of the top 10% most cited individuals globally. Currently Dr. Ronander is mainly retired and an extremely large shareholder.

Once Klydon was bought they went to work building out their company’s engineering infrastructure to be able to bring the technology to commercial use. Currently only 9 individuals are allowed to have access to the technology due to the lack of IP protection since most of their process is scientific “know-how” and technical expertise that can’t be found anywhere else. Six of these individuals are ASPI specific (not affiliated with Klydon), own stock in the company, and have 100% retention.

ASP Isotopes Methods of Enrichment and Technology

First it should be restated that not even the CEO has full access to the technology so I can merely go off of a semi-detailed report in the 10-K describing the ASP method. My understanding of this method could be missing key information. The quantum enrichment method seems fairly similar to laser method with minor (but definitely highly technical differences) that improves the process.

Aerodynamic-Separation Process Method

The Aerodynamic Separation Process, aerodynamically separates the molecule via a stationary wall centrifuge paired with proprietary flow directors to separate isotopes of varying levels of atomic mass. Similar to a gas centrifuge but without needing to move the centrifuge or have nearly as many stages. I would describe it as similar to rifling in a gun barrel that the molecules (usually gas) are sent through at high velocity. It is a much more capex efficient process than Gas centrifuge basically due to less moving parts.

More detailed technology review can be found at this study: https://klydon.co.za/images/asp_2012.pdf

Edit: I originally had a selectivity of 7 but it is actually 1.15 which is very similar to gas centrifuge.

Quantum Enrichment

This seems to be a variation of laser enrichment. The most important part is the selection process which has been enhanced by the company’s use of quantum mechanics to identify isotopes via their transition energy at extremely high heats in a vacuum (The high heat is only necessary due to the need for uranium metal to be vapourized - unlike Silex, the photoionization is not dependent on the temperature). Once identified they are hit with a laser and photoionized to be later electrically separated.

The QE tech seems to be AVLIS with an enhanced laser system. I don’t know if that means the laser penetrates the mass stream better, or it is less likely to excite U-238, or if the actual energy is different. In standard AVLIS the valence band of U-235 is excited in three steps, with the final step being the one that actually ionizes the atoms. When references are made to this 3-step excitation process, Paul cryptically says “it might be 3, it might be less”, so it is possible QE manages to ionize in only 1 or 2 steps.

This is all done in one stage which is not expected to be the case for Laser enrichment, which one of their key competitors utilize. QE utilizes metals, which means that uranium must use a different conversion system than what currently exists (current conversion technology converts uranium to a gas) that they will have to create at an industrial level for themselves. The selectivity for Quantum Enrichment for uranium is 678 vs less than 50 for Laser enrichment (both AVLIS and MLIS).

Nuclear Medicine

The first major field that will begin producing revenue for the company is the medical field. In October 2023, ASPI acquired 51% of PET Labs, a radioisotope company in the nuclear medicine sector. This will be their jumping point for the industry.

Carbon-14

Carbon-14 has already been contracted via a Canadian supplier that should begin delivering revenue any day now with margins in the 80% range and a minimum revenue of $2.5m annually. Carbon-14 was previously only produced by Russia and current supply chains are very ill-equipped. Carbon-14 is acquired from their supplier at a .5% enrichment and ASPI enriches it to 85% via their ASP technology. As I stated previously, this naturally occurs at one trillionth of a carbon molecule so the feeder stock comes from their customer (which is already enriched to .5% as a byproduct of another process) and the logistical issues are being solved to get this from Canada to Tennessee and back. This has caused some slight delays.

Molybedenum-100 and Molybedenum-98

Molybedenum-100 and Molybedenum-98 are not of particular use, but the isotope Molybdenum-99 can decay into Technetium-99 which is used in various scans (e.g., bone scans, cardiac stress tests) because of its favorable characteristics like a short half-life and gamma-ray emission, which allow for detailed imaging with minimal radiation exposure to patients.

Molybedenum-100 is extremely stable and is much better for transportation/storage and can convert to Molybdenum-99 (unstable with short shelf life) with a linear accelerator or a cyclotron but this process is regulated by the FDA (along with Canada Health and European Medical Agency).

The only country who has approved Molybedenum-100 to Technetium-99 via a cyclotron is Canada which means this will have to go through an FDA approval process for US usage. This is a $4.17 billion market. Outside of China the uptake of this will be very slow as the company seeks approval in the US and Europe in the coming years. Currently there is a contract with China starting this year of $2.5m-$27m per year. Technically the contract specified deliveries were to start in July 2023 so this contract could be a zero.

Zinc 67/68

Zinc-68 is used as a precursor in the production of Gallium-68, a positron-emitting isotope used in PET (Positron Emission Tomography) scans. Ga-68 is valuable for imaging in oncology, cardiology, and neurology. Gallium-68 is a $130m field. The facility (also the first Icelandic facility) used to enrich Zinc-68 will be up and running in August 2025. The initial customer for Zinc-68 is helping fund the capital investment for the icelandic facility and is expecting to start receiving products by August of 2025.

Nickel-64

Ni-64 is used to produce Copper-64 (Cu-64), a radioisotope that is valuable in nuclear medicine. Cu-64 is used in PET (Positron Emission Tomography) imaging and targeted radiotherapy for cancer treatment. It is particularly useful in theranostic applications, where it helps both in diagnosing and treating diseases. The date for when this will be up and running is TBA.

Ytterbium-176

Ytterbium-176 is the first isotope that will use Quantum Enrichment technology and production for that plant ends in August and production will begin in September of 2024 (nearly 9 months to a year ahead of schedule). Ytterbium-176 is a key stable isotope used in the production of Lutetium-177 (177Lu). Lutetium-177 is an emerging beta-emitting radiopharmaceutical used in oncology drugs such as Novartis’ Pluvicto. There are currently two FDA approved drugs and more than 66 ongoing clinical trials for drugs that require Lutetium-177.

Consensus forecasts for Novartis’ Pluvicto exceed $4 billion and the beta emitting radiopharmaceutical market is expected to exceed $15 billion per annum in the next decade. The TAM for this isotope specifically is about $100m at the current moment and could triple to $300m+. The supply chain for this radioisotope has been particularly challenged with recent industry reports highlighting over two months treatment delay due to lack of drug availability. The Company is in discussions with multiple potential customers and aims to start commercial production on Monday, September 2nd (almost a year ahead of schedule).

Since this will be the first use case of Quantum Enrichment it should lead to a smoother development of the Quantum Enrichment facility needed for Uranium in 2026/2027. The other good news is that this was built much faster than expected.

Nickel-64

Nickel-64 will be the 2nd isotope that will use quantum enrichment technology. Nickel-64 (Ni-64) is a stable isotope of nickel which is mainly used as a precursor in the production of Cu-64. Cu-64 is a radioisotope of copper with a dual capability of imaging and therapy. It has a half-life of approximately 12.7 hours.

Silicon Chips

The second major field that will begin producing revenue for the company is the chip industry.

Silicon-28

Silicon chips used for current chip manufacturing are made of 92% Silicon-28 (naturally occurring). Silicon-29 is not as thermally conductive as Silicon-28, hence allowing it to heat up more. ASPI believes it can enrich Silicon-28 to 99.996% Silicon-28 and remove most of the unwanted Silicon-29. This would be a boon to chip manufacturers and data centers that are trying to reduce their energy consumption as much as possible. Without any marketing, the CEO of ASPI has claimed that they already have customers contacting them to place orders. These new pure silicon-28 chips are expected to be 150%-300% more energy efficient due to a relationship in how nanowires work.

https://newscenter.lbl.gov/2022/05/17/silicon-nanowires-take-the-heat/

PLEASE TAKE ONE SECOND TO LIKE THIS POST

It is also beneficial from a quantum computing perspective. From their website “Naturally occurring silicon has three isotopes – 28, 29 and 30. The 29 isotope has a ½ positive spin, which is an intrinsic form of angular momentum carried by elementary particles. In contrast, highly enriched silicon-28 is spin-free where qubits are protected from sources of decoherence that causes loss of quantum information. In addition to its potential to process superior information such as qubits, it is believed that highly enriched silicon-28 can conduct heat 150% more efficiently than natural silicon, which will potentially allow for chips to become smaller, faster and cooler.”

ASPI will begin to produce this 99%+ enriched Silicon-28 by the end of this year. They believe their current production should be enough for Chip makers to test pure Silicon more in depth and should be able to handle demand through 2025. The first Iceland plant for Silicon-28 is expected to be finished in 2026 but this timeline could change depending on demand.

Earlier this year they announced 2 undisclosed contracts for Silicon-28 that will be produced and sold this year:

Silane

ASP tech is able to enrich silicon as Silane which is an actual usable form for chip manufacturers (unlike competitors such as Rosatom). From the ASPI website:

“ASP Isotopes’ proprietary technology can enrich isotopes of low atomic mass (such as silane (SiH4), molecular mass of 32), as well as isotopes of heavier masses. Other companies developing methods to enrich silicon generally either enrich silicon tetrafluoride (SiF4) or a halo silane. Neither of these chemicals can be used directly by a semiconductor company and require chemical converting processes that potentially harm the purity of the final product. By processing silane directly, the Company believes that its finished product will be of a higher quality and may be used by semiconductor companies without the need for additional chemical conversion processes.” ASPI believes they are the only company that can process Silane.

Nuclear Energy

Lithium 6/7

Li-6 is used in breeder reactors to produce tritium, an essential component in the fuel cycle of these reactors. Tritium is generated when Li-6 captures a neutron and undergoes nuclear reactions. Tritium is also used for Nuclear Fusion meaning that Li-6 is also used in Nuclear Fusion Tokamak reactors.

In Molten Salt Reactors, Li-6 is a key ingredient in the molten salt mixture, where it enhances the reactor’s efficiency and safety. It helps in the moderation of neutrons and in maintaining optimal reactor conditions. Lithium-7 is a separate component used in a different part of the process in MSRs. It enhances the thermal stability of the salt, ensuring efficient heat transfer and safe reactor operation..

Although not stated by the company, I believe that Lithium-6 could have real viability in the use of Solid State Batteries due to its diffusional properties which is the main bottleneck point for Solid State Battery technology but there is currently no cheap available product for Lithium 6. Naturally occurring Lithium contains 92% Lithium-7 and 8% is Lithium 6.

Current methods of enriching Lithium are disastrous and expensive and involve huge amounts of Mercury. ASPI believes they can enrich Lithium with a selection factor of 113 making it both a cheap and much more abundant material via QE.

Reading Material: https://world-nuclear.org/information-library/current-and-future-generation/lithium

HALEU Uranium Enrichment

Currently there is no enrichment facility for High-assay low-enriched uranium (HALEU) or basically Uranium enriched to 5%-20%. Their process can enrich HALEU to 19.75% in one stage. As the nuclear industry switches to focus on Small Modular Reactors (SMRs), which are cheaper, smaller and quicker to build, then the focus will turn to HALEU. HALEU is the only fuel that can be utilized by these SMRs. This will eventually turn into a $30b industry for HALEU fuel as the demand for SMRs continues to skyrocket. Current SMR companies were reliant on Russia for their enriched nuclear fuel needs, but this has since been impossible after the Russia enriched uranium ban. Building SMRs is a bipartisan issue with both Kamala Harris and Donald Trump coming out in support of building more SMRs. Russia is also not able to compete on cost with ASPI’s quantum enrichment method.

The company will be the first of possible 3 companies in the world to provide this needed nuclear fuel and the company is convinced that they will be able to produce it cheaper and more efficiently than any of the other companies in the world.

From the company’s website:

“Currently there is no Western producer of HALEU and the US NEI (Nuclear Energy Institute) predicts a global shortage of 3,000 metric tons by 2035. We are currently in discussions with several SMR companies requiring HALEU and we already have indicated demand of approximately $30 billion, at current fuel prices. We believe that the two year old NEI estimate significantly underestimates the actual market demand.”

Bill Gates and his company Terra Power referenced his reliance on HALEU. He essentially called out the company in the article below as “suppliers from the UK and South Africa” when referring to the new HALEU companies they will procure from (there are no other HALEU companies in the UK or South Africa).

From the article: “One issue the project initially faced was that the uranium fuel would need to come from Russia. Gates noted that the project was delayed from 2028 to 2030 because of the fuel supply, with Russia's war against Ukraine changing the calculus. But suppliers in the United Kingdom and South Africa, along with an eventual supply from uranium mines in the U.S. and Canada will allow the project to go forward, he said.” Beyond that, the company reports that it has assigned two existing memoranda of understanding (MOUs) with U.S. based small modular reactor companies for HALEU in February of this year.

If we assume $25,000 kg/HALEU by 2026 and we use the above demand chart we come up with below dollar demand per year. This demand per year assumes TAM for each year for the enrichment process specifically (enrichment is roughly 33% of the cost of enriched nuclear fuel). I believe that gross margins for uranium enrichment will be 60%-70%+.

HALEU Total Dollar Demand by Year (Assuming $25k/kg of HALEU)

By 2027 the company is expected to be in full production of HALEU and able to produce the entire world's HALEU needs due to their high selection factor. They will test out the technology via their Ytterbium-176 facility which should help in the creation of the uranium enrichment facility and other future QE facilities (Nickel and Lithium).

Another thing to note is that due to the extreme efficiency of their Quantum Enrichment, it is likely that the company could be able to compete for Weapons Grade Uranium (WGU) contracts (which is likely a large contributor to why this part of the business will be spun off, more on that in a later section). WGU requires 90%+ enrichment and is highly regulated. Since HALEU already has 85%+ of the energy requirements to get to WGU, it is likely that the company could receive contracts for WGU. Also of note is that the company is looking for CEO/s for QLE in the US and UK that have military expertise (this article was written before the most recent hiring for QLE UK, which was a fantastic CEO hire). This has not been publicly stated and is merely speculation by myself due to understanding of HALEU in terms of enrichment processing.

It should be noted that the UK navy will be in a shortage of WGU for nuclear subs in the 2030s and QLE will be able to help address this shortage.

ASPI believes they can be profitable well below $10,000/kg implying gross margins of well above 70% at current prices. ASPI will be able to produce enough HALEU to address all global needs. This implies a revenue of $600m at $25k/kg ($165m per 20mt). This amount will be rapidly ramped up based on additional HALEU facilities in the UK (which should begin working on the license process in 2024/2025), South Africa (which should be licensed this year), and the US (TBA).

The initial facility will be able to process 20 mt of uranium by 2027 but this can be rapidly expanded or reduced due to the modular plant construction model of their facilities. The CEO is under the impression that they will be able to meet all HALEU demand by 2028 of 100+ mt of uranium per year.

To read more on the Uranium Industry’s coming dire supply situation, please review my Part 1, Part 2, and Part 3 articles that can be found on the Rogue Funds Blog.

Nuclear Waste Re-Use

The company believes that due to their high selectivity they will be able to reuse nuclear waste from past enrichment to create HALEU. No other company will have this ability (Silex says at best they will be able to produce LEU from this waste not HALEU). After a company enriches uranium it leaves nuclear waste (not toxic waste from reactors) and it is well below the natural uranium-235 enrichment of .7%. Most companies will give them this uranium waste for free or might even pay them to take it. This should allow them to produce HALEU at highly competitive prices with extremely large margins.

It is unlikely that any other competitor will be able to do this. This would further increase their competitive advantage. There are roughly 1.7m metric tons of these “depleted tails” in existence.

Competitors

Centrus Energy

Centrus produces HALEU via Centrifuge Enrichment as described in the section on enrichment methods. This enrichment is obviously much more expensive due to the cascading centrifuge model and most likely does not consistently produce 20% HALEU or even close to that level. As of 2023, they have produced 0.9 metric tons. They are unlikely to be a serious competitor as they will struggle to get enrichment up to 20%. They will be a serious competitor in anything involving ASP technology.

Silex

This seems to be the main competitor of the company in the future. Silex has lagged ASPI by a few years and currently trades for $650m. They currently use some variation of Laser Technology (MLIS).

ASPI believes that they will be able to outperform them due to their high selectivity via Quantum Enrichment. This higher selectivity will allow them to perform enrichment in one stage instead of a cascade of lasers. This will mean a cheaper final product. Silex is a joint venture with Cameco, which is the second largest producer of Uranium in the world. The company is owned 49% by Cameco with another call option to buy 25% of the company at fair market value. Their facilities are not expected to hit commercial viability until 2029 or later for uranium (1+ years after ASPI) and 2027 or later for Silicon and Ytterbium-176 (3-4 years after ASPI). Silex will be a realistic competitor, but it is likely that APSI will take up a much larger market share due to better technology and first mover advantage. They key thing to note is that they will be focusing much more on LEU production, especially in the early days of commercial production. It is highly unlikely that they will have any serious focus on HALEU production.

For comparison: Silex is expected to have a selectivity of less than 20 and QLE is expected to have a selectivity of 678 for Uranium (although I would expect less than this at commercial levels, it is unlikely to have a true meaningful impact on their ability to create HALEU). This is a huge deal when it comes to the cost of enrichment for HALEU and the ability to enrich WGU. Although Silex is under patent and DOE safeguards, the company knows what technology they are using because they sold them the lasers needed for enrichment. Most of their patents and protection are purely because the US enforces very strict regulations ensuring secure facilities. For example when ASPI creates a US entity to enrich uranium then the current ASPI CEO, QLE UK CEO and anyone else not part of that US entity (which has to be ran by an American) cannot step foot inside the facility even though they already have the technology created in South Africa (Gotta love government regulations). It is unlikely that they will be a competitor in Lithium production or other lighter isotope technology.

More info on Silex tech: https://www.tandfonline.com/doi/full/10.1080/08929882.2016.1184528#abstract

Urenco

Their method of enrichment is centrifuge, similarly to Centrus Energy. Urenco will be able to supply low weight elements (such as silicon, zinc, etc.) but not to the production levels that ASPI will be able to. They are also building a facility for HALEU which will be available (at the earliest) by 2031. Their total production capacity will be 10 MTU’s. ASP should be able to produce larger margins at cheaper prices once the Iceland facilities are in place for their ASP tech. This will be less than 5% of total estimated demand in 2031. I do not believe they are a serious competitor. Urenco is the only other company that could address the UK WGU shortages but it is their bylaws that they will not produce WGU (also they don’t compete well on cost).

Rosatom (Russia)

This is the leading supplier of the world's enrichment needs for Low Enriched Uranium (LEU). With the dissolution of the Soviet Union, Russia became the leading supplier of the world by flushing the US with cheap WGU that could be diluted into LEU. This put most enriched uranium suppliers out of business leaving Rosatom with huge market share. Once the supplies dwindled, Rosatom maintained market share via centrifuge technology and has maintained that even through today. They do not produce HALEU and have no capacity to enrich uranium commercially outside of centrifuges. Rosatom does enrich many other isotopes (such as Ytterbium-176, Carbon-14, etc.) which have all been disrupted due to sanctions. If/When Russia becomes more involved in the global economy in the coming decades, it is likely that Rosatom will become a competitor for lighter isotopes. I expect that Rosatom will not be able to effectively compete in the heavier isotope industry due to their use of centrifuge technology.

Insider Ownership and Incentive Structure

The CEO (Paul Mann) is the second largest owner of the stock with 10% of the stock. All insiders, including Mann, add up to 36% since the company’s and members continue to buy shares. Insider ownership and buying is a huge green flag with the company.

Mann is paid a $500k salary with additional bonuses for up to 100% of the salary. The below incentive is extremely interesting and I think it is ideal for a company that operates on the margins that ASPI does. Mann is essentially paid a $1m bonus for every $4m in increased monthly revenues going up to $16m monthly. This is ideal for a company like ASPI that operates on margins north of 70% and needs to rapidly scale their business. See below for the exact statement on the incentive:

“Subject to our achievement of $4.167 million in average monthly revenues for a trailing three- month period Mr. Mann will be paid a $1,000,000 bonus. Subject to our achievement of $8.33 million in average monthly revenues for a trailing three-month period Mr. Mann will be paid an additional $1,000,000 bonus. Subject to our achievement of $12.5 million in average monthly revenues for a trailing three-month period Mr. Mann will be paid an additional $1,000,000 bonus. Subject to our achievement of $16.67 million in average monthly revenues for a trailing three-month period Mr. Mann will be paid an additional $1,000,000 bonus. Any earned milestone-based bonuses will be paid within 30 days of the achievement of the applicable revenue goal and the number of vested shares issued to Mr. Mann shall be determined by dividing the $1,000,000 bonus amount by either the then fair market value per share of Common Stock, as determined in good faith by our board of directors, or the closing sale price of our Common Stock on the trading day immediately preceding the applicable payment date, as reported by the principal trading market for our Common Stock.”

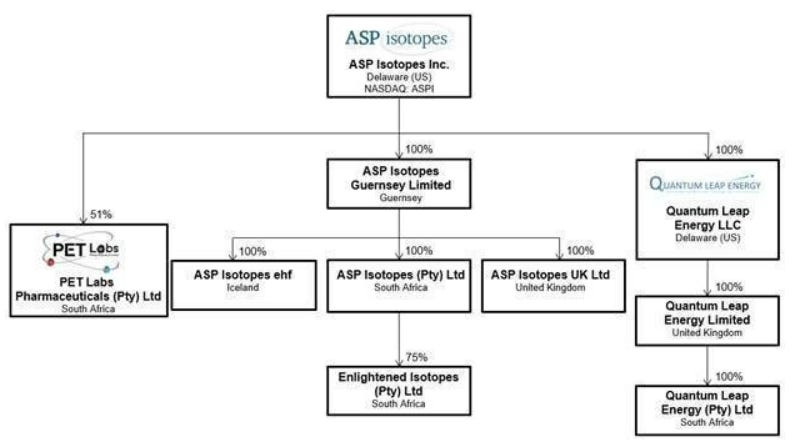

Company Structure

Currently the company operates under the above structure. The company plans to spin off Quantum Leaps Energy (QLE) in a 1 for 1 spinoff (1 share of QLE for each share of ASPI). Essentially, they are valuing QLE as equal to the rest of the company ($75m valuation for each half of the company = $150m total based on the market cap). They were originally going to IPO QLE but decided against it and then decided to capitalize the QLE via the most recent public offering (which cratered the stock). Now that the company is capitalized it will be spun off into its own entity with its own independent board of directors. The rest of the company will continue to operate under ASP Isotopes.

The spinoff is most likely due to the nuanced industry differences between uranium and the rest of the company. As you read above, I believe that the current QE technology is most likely a viable way to efficiently (read cheaply) achieve Weapons Grade Uranium (WGU) and the ASPI side of the company has a contract in place to sell Mo-100 to China (although this contract could be dead for now). I believe that this dynamic could contribute to the company’s idea to spin off QLE, which will deal in a highly regulated industry. After the spin off ASPI will receive a 10% royalty from QLE when the spin off is complete.

Regarding PET lab, ASPI has an option to buy the other 49% of the company (currently owns 51%) for an agreed consideration totaling $2,200,000. Dr. Gerdus Kemp controls the remaining 49% ownership of PET Labs Pharmaceuticals and is an employee of ASP Isotopes. The remaining balance for the 51% acquisition is $1,235,250 and is expected to be paid in November 2024. If PET labs proceeds to be as profitable as expected (especially with Ytterbium-176), then I would not be surprised for the rest of the company to be bought out next year so that ASPI will have a vertically integrated PET company.

Facilities

The company currently has multiple facilities in South Africa but is beginning to build out a “cluster” of facilities in Iceland where they will finish their first facility next year ($30m in capex that is mostly customer funded). The reason for this is the cheap energy from geothermal energy in Iceland makes it ideal for the various enrichment facilities and reduces costs as much as possible. I believe that in the long term this will be a competitive advantage compared to other enrichment facilities to keep costs low, as Iceland is expected to reduce energy costs by up to 85%.

Initial HALEU facilities will be built in South Africa due to a faster license attainment process. The UK will be a target for QLE facilities (and uranium enrichment) immediately following the South African facility. Eventually the company will have facilities in the United States for QLE but licensing has slowed down the process and they want to go to market as soon as possible, so the US will be a future location as well.

The Company is currently building three plants in Pretoria, South Africa: a Carbon-14 plant, a multi-isotope plant and a laser isotope separation plan using quantum enrichment technology. The Carbon-14 plant was completed in June 2024 and depreciation for the plant will begin in July 2024. The QE plant will be completed by the end of August and in production by the end of September (again, almost a year ahead of schedule).

PPE from latest 10Q

Valuation

Currently the company is “pre-revenue” with C-14 contracts supposed to hit any day now. The following 5 months should have various contracts hitting and the CEO expects cash flow positivity before year end. The company currently has various contracts in place that we know are roughly as follows:

- Chinese Company Mo-100 contract worth ~$2.5-$27m. (annually). Should be noted that this contract might be a zero.

- Canada C-14 contract worth $2.5m. (annually)

- Undisclosed enriched Isotope contract worth $9m.

- Undisclosed Nuclear Fuel research worth $2m.

- $2m in current PET lab revenue

- Two Undisclosed Si-28 contracts. They have completely sold out of their Si-28 production via these contracts. I believe pure Si-28 sells for $500k per kg and they have sold out their 10kg of production. This most likely means ~$5m from Si-28.

PLEASE TAKE ONE SECOND TO LIKE THIS POST

Alright, so let’s take the worst-case scenario of these contracts. This is roughly $20.5m ($0m + $2.5m + $9m + $2m + $5m (estimated) +$2m). The gross margins for this $20.5m are probably 70%. Let’s assume they get 70% margin then add SG&A expenses (which are slightly bloated due to public raise costs and delaying SG&A payments at the first half of this year) around $10m. This leaves us at cash flow of $4.35m or very near cash flow positive with just current contracts. This does not include the Ytterbium-176 facility that will be finished on September 2nd, or the Zinc iceland facility that will be in production next August. Future Nickel and Lithium facilities depend on licensing but there is a high chance we see those facilities before 2026. PET Lab contracts are also supposed to continuously increase.

Since most costs are now fairly fixed I would expect roughly double this revenue in undisclosed and future contracts through summer/fall of next year. This would make revenue of $40m-$60m and EBITDA of ~$15m-20m+ if we assume 40% operating margins. This is probably a very conservative guess at the actual EBITDA with the very likely chance they pick up even more contracts over the next 12 months. So, the current conservative valuation implied by the stock market is 10x estimated 2025/2026 EBITDA. This is only focused on the ASP section of the business. This is a ludicrous valuation for a company whose product is so in demand that they haven’t even had to market their isotopes.

The reason the company is trading at its current valuation is because the CEO is running this company like a biotech company. They have been diluting with little concern of shareholders to try to get operations running as quickly as possible. In the long run this will be a great strategy for them to grab and secure market share, but it has been a rough strategy on the stock in the short term. The CEO mentioned in the annual letter to investors in April that when the company begins to produce cash flow (which is this winter) and it is the expectation that future funding will purely be via debt and the company’s own cash flows. The CEO has said multiple times over the last 2 months that they have no future plans of diluting and that SG&A increases should slow significantly from here due to finished internal infrastructure of building out a corporate office and all of the necessities needed for being a growing public company.

Since QLE is no longer going to be IPO’d, this raise was purely to adjust for that change and capitalize the company. Shareholders who sold on this raise will miss the opportunity for the spinoff of QLE which I believe is highly valuable under a rapidly increasing TAM with a monopoly/duopoly control on a TAM of $8b+ in just over a decade. We know that ASP Isotopes and Pet Labs will be cash flow positive by the end of the year. So the rest of the valuation drain will likely come from QLE allowing for a spin off to be highly accretive for ASPI in the short - medium term. But in the future the 10% royalty from QLE will be highly accretive and beneficial for ASPI as well as QLE.

There seemed to be some lagging correlation between Uranium and ASPI that is now much more in sync. The spinoff of QLE should allow for a revaluation and separation from its current uranium identity.

I believe the market is making a huge mistake in the valuation and that it is likely that the company will rapidly increase their contracts over the next 18 months as they actually begin to produce cash flow and products. There is an extremely high likelihood that by the end of 2025 they will have over $100m-$150m in annual contracts putting their valuation at $1.5b+ (or 15x-25x FW EBITDA). This is not to include the current ownership of QLE which could have a valuation that goes for much higher depending on SMR demand for HALEU.

If we take current demand estimates for HALEU for 2027, with 60% market share in 2027, net income margins of 30%-40%, and an earnings multiple of 20x, then we end up with a valuation of $3b-$4b for both companies combined. The demand for HALEU will only grow from there and it is likely we could see a valuation going well above $10b based on the company’s performance in 2030. Obviously this is speculation but it shows the fantastic opportunity available for the company and the huge margin of safety in the coming years.

I also believe that as they produce larger production facilities for Si-28 that almost all chip makers might focus on having a more pure chip if the company is able to get costs low enough to make the efficiency savings worth it for most fabs. This will be a long run trend to observe and will most likely move very slowly.

I believe that over the next 5-7 years we could see contracts between $500m-$2b+ for both companies combined (and I believe this estimation could be highly conservative), this would align with valuation of current competitors. This would give a valuation of well over $10b in the coming years for the 2 companies combined ($130/s+) if the competitive landscape stays the same and SMR demand maintains. Of course as production hits in the company over the next ~3-4 years we will have a better idea of the long term valuation. This gives a massive market opportunity of 55x+ from the current value of the stock. Based on next year's speculative contract estimates, we could see a valuation of $1b ($13/s) as early as 2025.

Risks

Short Report by J Capital

A short report for ASPI was written earlier this year which I will address here:

- The first concern was that Mann served as CFO for PolarityTE which was written up as a short report by Andrew Left and the company was investigated by the SEC. This is completely irrelevant as Mann was hired as CFO on June 21st, 2018 and the short report came out on June 25th, 2018. The SEC only investigated the company in the years 2013-2018. There was also nothing found by the SEC, Lefts report was shot down by most experts, and Andrew Left is now under investigation for market manipulation.

- The short report then addressed the company’s lack of patents. This has been discussed by the CEO numerous times due to the creation of a similar technology in the 1980s by the South African government and has now been perfected due to scientific know-how and trade secrets. They acquired the ASP technology rights from Klydon in 2023. The facility where they operate is extremely secure but stationary centrifuge isn’t a new concept, their expertise and know-how is what allows them to enrich isotopes better than anyone else. They have 100% employee retention, which has allowed them to maintain trade secrets.

- Jonathan Honig, brother of Barry Honig (known stock promoter) owns a bit of the company. He is far from a significant shareholder at the current moment and this is irrelevant.

- The short report asks why the company is based in South Africa which makes it a suspicious company. It’s because the company they bought is out of South Africa and its facilities are there. They are currently building out facilities in Iceland and will begin construction in the UK in 2025/2026.

- The report calls out that the company has zero revenues (while it builds out its commercial enrichment facilities). This will be answered in the next 2 quarters.

Frankly, I have never seen a CEO or Board members (some who are dipping into their own cash beyond salary) buy a company’s shares, which is an “obvious fraud.” I think this short report is completely wrong in its assessment.

Technology Failure of Quantum Enrichment

Quantum Enrichment technology could fail but this seems highly unlikely since it seems to be fairly similar although more accurate than Laser Enrichment. I think this is extremely unlikely, but we will know this month if it can enrich Ytterbium-176 (production begins on September 2nd). Based on the highly skilled research team and the fact that they are already putting money into commercial production (along with insiders buying the stock) it seems very unlikely that this technology doesn’t work. The bigger risk is that production gets delayed from license issues.

The current order for quantum enrichment production is Yttberium-176, Nickel-64, Lithium-6/7, Uranium-235.

Further Dilution

I believe that ASP has most likely seen its last large raise based on this statement from the CEO and this raise being directed at capitalized QLE:

“We have a large backlog of interest from customers for many different isotopes and we expect to fund future isotope enrichment facilities using primarily funding provided by those customers combined with additional debt. With proof of concept for the ASP process now demonstrated and revenue generation from the sale of enriched isotopes anticipated this year, we have begun discussions with multiple potential debt providers.”

It seems that a debt deal going forward seems much more likely once the company gets revenue and cash flow up and running efficiently. Even QLE seems fairly unlikely to get further dilution from here since the main point of this offer was to avoid the IPO of QLE and just spin it off. Insider ownership from here on out should limit the amount of dilution to a decent amount. The CEO last month said they do not expect to do any more cash raises. The CEO also said they do not expect to do any dilutive raises on their latest earnings call.

Stock Based Compensation is high with the current CEO contract at 2% of shares being given to him in Stock Based Compensation. Other executives will probably maintain similar standards. Current shares diluted are 73.3m.

South Africa is volatile and has had historic electric power issues

This is easily the largest and most likely risk until their Iceland facilities are up and running and they get licenses to enrich Uranium in the US and UK. They do have a backup 1.5 megawatt diesel generator which is an extremely large generator and could most likely run most facilities. Iceland should be up and running with numerous facilities within the next couple of years and the short-term risk is still extremely extremely low. This risk is not a long-term risk due to the Iceland facilities and future UK and US facilities.

Nuclear Government Funding for Enriching Could Create Unknown Competitors

As governments around the world pick up interest in nuclear energy, if a bottleneck is created this could lead to new technologies or new companies that are funded by huge government sums that the private industry could not hope to match. This could cause a proliferation of new competitors entering the industry. I find this to be unlikely due to the regulation and time to build a commercial size enrichment facility, it would take many years to catch the current market leaders. These markets are also huge and ASPI will retain a large part of the market for the foreseeable future.

Delays in Timeline

The company could experience delays in the timeline of production. I believe that this will be minor blips in the long-term direction of the company. Their QE technology has actually seen an acceleration of almost a year and it would be great to see that translate to its future HALEU facilities. Their current timelines almost all depend on license approvals.

Failure to Ban Russian Imports

I believe that this may be something we will see in the short term as there are no other competitors in the market for western countries to turn to. As ASPI builds up their global presence to address the shortcoming of western isotope enrichers, they will be the clear favorite for most western countries to deal with. While there is a void (specifically for Uranium) it will not be surprising to see that somehow Rosatom exports illegal enriched LEU uranium shipments in the short term. These shipments shouldn’t have large impacts on ASPI.

Large Price Increases in Uranium could price out small Mini Reactors

Although most SMR’s should be relatively price inelastic when it comes to the price of Uranium the mini reactors should be much more price sensitive. This type of sensitivity could cause issues to future HALEU demand depending on if the industry moves towards smaller and smaller reactors. This shouldn’t be a huge concern as most SMR companies are building reactors greater than 150 MWe (Terrapower is 350 MWe) and this equates to a $2b-$4b reactor and $120m+ in annual operating costs with HALEU being about 15% of annual costs (compared to the 2%-4% cost of nuclear fuel in a large scale reactor). If HALEU prices were to double or triple this could increase annual operating expenses immensely for these smaller reactors and we could see an adjustment in HALEU demand. The other risk mitigating factor regarding HALEU demand is how subsidized SMR’s are expected to be.

Technical Expertise could be Replicated

SP tech doesn’t seem that complicated. I think a well funded team of top engineers (especially with AI in circulation) could potentially reproduce the tech in a relatively short time. QE could be harder, but could still be similarly vulnerable. With current licensing time frames, technical expertise, and top security this is no closer than a decade away in my opinion.

Conclusion

This risk/reward seems like an absolute no-brainer, and it seems like executives are in the same boat as they continuously buy the stock. I believe a 10 bagger in the next few years is highly likely, especially when comparing their valuation to competitors, with a possible 100+ bagger in the next 5-7 years a real possibility. Their competitors who have worse technology and have been horribly slow to scale (Silex took 18 years to get a license) are trading at 3-5x their ASPI’s current market valuation, which makes little sense.

The catalysts are the QLE spin off will make ASP Isotopes look like a much better company. South Africa should be approving HALEU licensure before 2025. With dilution behind them it seems that the company is significantly derisked with extremely high demand on the horizon. Obviously QLE is quite a ways off from production so they will be a drag on the company until that spinoff which will unleash how great the ASP tech is on its own. Over the coming years the QLE company will become its own behemoth to deal with and should be a long term boon for the company. The two entities in combination could possibly lead to a total 100+ bagger for this investment in a relatively short time frame (less than 10 years).

The other catalyst is the high short interest on the stock (20% of float, with long term share holders taking up 40%+ of shares outstanding this is likely closer to 30%+) which could lead to a short squeeze if both revenue and cash flow begins to ramp up towards the back half of this year. When the next multi-isotope facility finishes at the end of this year we will most likely see a huge swing in the trajectory of the stock as the company switches to cash flow positive (combined with the QLE spinoff). There are very few negative catalysts over the next 18 months that could slow the upward pressure of the stock.

Disclaimer: The author of this idea and his Fund have a position in securities discussed at the time of posting and may trade in and out of this position without informing the reader.

Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

This article may contain certain opinions and “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential,” “outlook,” “forecast,” “plan” and other similar terms. All such opinions and forward-looking statements are conditional and are subject to various factors, including, without limitation, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors, any or all of which could cause actual results to differ materially from projected results.

Congratulations on a great article, and being the first to mention ASP Isotopes on Substack. This will be one for the ages.

A very good DD article about an extremely compelling opportunity. They recently proved out their QLE technology so that is one less giant risk. If they can do it for Lu-176 then they can do it for anything now! It is just a matter of scaling and execution which will take a few years but I am patient considering the good chance to 10x eventually. Not looking too far into the future yet.