ASP Isotopes: A Thoughtful but (Very) Long Response

Please View the Disclaimer at the Bottom of the Post

This isn’t how I planned to spend the day before Thanksgiving, but here we are.

I felt I had an obligation to my limited partners within my Fund to give them a detailed response of why we have not sold a single share of ASPI since the report and will continue to hold despite recent volatility and the recent short report. The more I wrote the more I realized I should share this report publicly. This report will be written over the following days as I organize my research into this comprehensive report.

I am not a nuclear expert and my science background is merely that of a mechanical engineer. I have read many scientific papers and literature on nuclear enrichment at this point but I may mistakenly utilize some concepts. I feel the knowledge I have shared is mostly accurate to the best of my knowledge and I have talked with multiple experts in the field who I have walked through my thought process with over the past few months. Where I think I could be wrong or I am more hesitant in my thought process I will inform you, the reader.

Some concepts may be hard for some to comprehend so I highly suggest reviewing my first article of ASP Isotopes:

I will breakdown my report into two parts. First, a very long response to the most recent short report on the company, going roughly claim by claim. The second part will involve the technology ASP Isotopes uses, what the short report missed (including real risks), and why we continue to hold stock in the company.

Initial Reaction

Of course, my initial reaction was a knee-jerk one that this report was extremely similar to another short report that was released earlier this year. My initial response was that this is frankly missing a lot of key information and it shouldn’t be taken seriously. I then reread the whole report and came to new conclusions. The report brought up some questions I hadn’t thought of. It’s always a good thing to question your thesis and I try to rarely get married to my positions as I have investors who rely on me being right on a consistent basis and if I am wrong I need to accept that and not be the investor who buys all the way down.

Of course, I could be completely wrong in my following analysis! I have been wrong before and I will be wrong again.

After reading the report I had key red flag questions such as:

Who are all of these anonymous sources? Are they anyone of actual significance, if so then I should be extremely concerned.

Why does management have the wrong location on these smaller subsidiaries?

Wow a nuclear physicist from Los Alamos is highly interesting, and he says their laser technology doesn’t add up? This is something I need to look back into.

They clearly did some research (albeit with a ton of bias and cherry picking) and I will have to ensure complete clarity on everything.

What the hell is this writing style?

We’ll get to all of these questions in due time. I think the way I want this report to go is to directly address each concern brought up in the short report. I will then highlight what was missed by the report and then follow it up on additional risks that I have identified since my last report.

Response to Claims

So the largest and first claim was the connection of Barry/Jonathan Honig and John Stetson during the pre-IPO which identifies them as an indicator of fraud. Shout out to JCapital who wrote the original short report on the company and found this connection in February of 2024.

I am going to be frank. It seems very evident that Paul knew who Jonathan Honig was and his background. The SEC found he was not a character of wrong doing (according to the short report). As far as the “secretive shell” Dominari Holdings, at the time of their investment no Honig figures were in the capital structure. The photo they used was from 2014 with a claim that “we believe they are still running the show” (7 years later in 2021) with little to no evidence in support. Of course, it is better to be safe than sorry and this was still mainly involved in pre-IPO funding (and doesn’t look great).

I am assuming that Paul was extremely desperate for cash in the midst of COVID and reached out to anyone he knew to fundraise. At one point Jonathan Honig was the second largest shareholder and they sold out on IPO (which wasn’t exactly a splash hit IPO).

PLEASE TAKE THIS TIME TO LIKE THIS POST

The good news is that they don’t seem to be part of the company anymore (I noted as such in my initial post on the company) and Paul stated so on the recent Canaccord Genuity call. Paul has stated that he had not talked to John Stenson before or after his wife’s investment in the 2023 raise. He does not believe she is still invested because according to Paul they never reached out to him.

It should be noted that management and directors have never sold the stock and a large amount of open market purchasing has occurred over the past year. Management is involved in most raises (except the last one I believe, which was fairly small). This is frankly not characteristic of most pump and dump schemes. But this early ownership from shady figures will have to be overcome for any would-be or current shareholders.

Paul Mann PolarityTE Connection

This was from my original post on ASP Isotopes:

The first concern was that Mann served as CFO for PolarityTE which was written up as a short report by Andrew Left and the company was investigated by the SEC. This is completely irrelevant to Paul Mann’s time there as Mann was hired as CFO on June 21st, 2018 and the short report came out on June 25th, 2018. The SEC only investigated the company in the years 2013-2018. There was also nothing found by the SEC, Lefts report was shot down by most experts, and Andrew Left is now under investigation for market manipulation.

Again, this was brought up by JCapital’s short report. Anyone who has done any research into the situation would know Paul came after all allegations. Paul said he left as CFO due to a lack of cost cutting and disagreements with the board and decided to go back into investing. Again, the SEC did not find anything in the investigation.

Virtual Offices in the US Claims

This wasn’t exactly a hidden secret to anyone who has talked to management or done any research into the company. I would assume most individuals who have done research into the company know that all operations are in South Africa and Paul merely travels around the world for meetings with executives. The company works out of South Africa but is targeting the US for many key operations and are listed on the NASDAQ. The company eventually has a goal of building out offices in NYC. It’s hard for me to particularly care about these claims.

Lack of evidence for Subsidiaries

To begin with, the companies facilities do in fact exist. A good friend of mine visited South Africa last month with about 20 other investors where he saw all facilities. They could not view the technology in operation for obvious reasons but they were sitting there idle.

As you might notice, the report did not comment on most subsidiaries for very obvious reasons. If the short report team contacted ASPI then I am sure they would have no problem giving him or anyone else who would like a tour. As far as the other subsidiaries go, it’s frankly bad paperwork but it’s nothing I am losing sleep about. ASPI in their current growth stage has had a poor history of turning in their 10-K’s and 10-Q’s on time and I hope this report will be a wake-up call to ensure all paperwork is filed properly.

Investors can go visit the facilities and see for themselves. In January the company has an open invite to investors which you can view via this press release.

They are paying for stock promotions

The report addressed them paying for an IR firm, Red Chip. Paying for an IR firm isn’t a new thing but I will say some parts of Red Chip are a little cheesy and/or pumpy. This relationship ends towards the beginning of next year when their contract runs out. The things they announce though tend to be things that come from Paul and/or ASPI directly. They don’t just make things up (such as FCF positive in 2024 was a statement from Paul, more on that later).

Emerging Growth Conference is another firm that Paul works with (he seems to switch every other month doing an investing presentation between Red Chip and Emerging Growth Conference). The short report highlights the $7500 they pay per quarter ($30,000/yr… this is essentially nothing). I don’t think this is a great investment to be frank but with the lack of interactions it’s hard to believe this is causing the stock to be pumped. I will say I have found good information presented by Paul in these presentations. The below is the website where the short report claims “ASPI is prominently highlighted” (I highlighted them in red).

The claim against Ocean Wall seems to be reaching to say the least. The company received 50% cash and 50% QLE convertible notes (which is essentially a bet on QE technology). This is CEO, Nick Lawsons comment on the report:

We don’t publish paid for research in fact we don’t publish recommendations. Our work on ASPI was based in 5 years of independent work on the fuel cycle. We are paid by ASPI for two things:

1. Corporate finance

2. Asset raising

Every deal we have done we have asked to be paid in specie so we are aligned to the success of the company not for promotion.

Now we get to the fun part of the short report where more “serious” allegations were thrown about the technology itself:

Former TerraPower Executive(s) said the announcement was not serious and ASPI was bottom in terms of quality

The claims in this part of the report focus on the fact that this is not a purchase order and that it is not a binding agreement. First, lets address that this is not a purchase order. True, it was not a purchase order but TerraPower agreed to give ASPI $2 million for R&D purposes that was triggered by the NESCA MOU. TerraPower doesn’t seem to have a history of announcing purchase orders in general but in comparison to their other press releases this one seems to be fairly serious (I suggest readers go and check out the TerraPower news website for themselves).

ASPI should recognize some revenue from this $2mm contract in this quarter (not the whole $2mm). As far as it not being binding, we really have no evidence either way. The contracts haven’t been released by either company. In prior ASPI reports, it was referenced that ASPI had MOUs with two SMR companies, one of which was clearly TerraPower (as I suspected in my first article on the company). Then they released this “term agreement” along with TerraPower, which allows me to make a logical deduction that this agreement was more serious than an MOU. This seems much more serious than the Centrus MOU press release (which was clarified as an MOU meanwhile the ASPI/TerraPower agreement was clarified as a Term Agreement). You can see the beginning of both press releases below and I’ll let you make a determination:

Now lets talk about this “former” TerraPower executive(s). I addressed the first claim discussing that this is only an MOU. On the second claim regarding the fact that ASPI does not have a HALEU manufacturing facility, it should be noted that no other competitor has a truly commercial HALEU facility. Centrus has a very small facility that they have struggled to complete and still need to deliver the 900 kgs of HALEU that they agreed to give the DoE. To deliver truly commercial amounts of HALEU they probably need about $4b+ for 100 MTU, which they can’t fund themselves without huge debt issues. Not to mention it also takes them nearly 4 years of construction to produce a mere 6 Metric Tons of Uranium (MTU) per their estimations. Silex currently has no active commercial facility for LEU or HALEU and have no plans of producing HALEU until the mid-late 2030s per their CEO.

EDIT: The reason for Centrus not being able to completed their 900 kg facility (.9 MTU) is because they can’t get the required cylinders from the DoE due to delays.

But in relation to ASPI, they signed an MOU with NESCA (South African Nuclear Energy Corporation aka the Government) to build this TerraPower facility a few weeks ago. This is a fairly concrete plan to build a HALEU facility (no one else even has a solid plan to build a commercial HALEU facility). This also clearly has South African government partnership giving it another notch of clout (as South Africa produces the laser experts of the world, more on this later).

I would compare this NESCA agreement to BWXT’s agreement to manufacture HALEU feedstock for advanced reactors in the US.

Now, on the last claim regarding that this tech “is optimistic and not real”, this is where something funny is evident when you get more details on this executive. There are exactly 4 executives and 2 lawyers who have seen the ASP Isotopes facilities and have also worked with ASP Isotopes from TerraPower according to Paul Mann. Not one of those executives have left TerraPower. All of these individuals are NDA’d. So how this “former” TerraPower executive was able to make that third claim, is beyond me.

To address the rest of the report, I think we need to gather a better understanding of some of their main competitors.

Enrichment Competitors

Centrus Energy

Throughout this write-up you will get a very good idea of the landscape of the US enrichment industry and right now the only licensed HALEU producer in the US is Centrus. Centrus began in 1992 as a State Owned Corporation to enrich uranium called United States Enrichment Corporation (USEC). It worked on technologies such as SILEX, AVLIS, MLIS, Centrifuge technology, and Gaseous Diffusion. In 1998, the US spun off USEC to become its own private company which IPO’d in 1998. At this point the company decided that essentially all laser tech was doomed to fail commercially and either canned or sold most parts of their business. After shutting down the Lawrence AVLIS program (more on that later) they terminated funding of the SILEX program. I thought it would be ironic to utilize one of the articles that the short report used to determine that “AVLIS has left the building” that discusses this very topic:

U.S. interest in laser enrichment methods did not immediately die with the AVLIS program. In 1996, USEC had invested in the separation of isotopes by the laser excitation (SILEX) technique being developed in Australia. The U.S. and Australian governments demonstrated further interest in the project on June 20, 2001, when they announced that they had officially classified the SILEX method. But USEC's interest in SILEX proved short-lived, and on April 30, 2003 it terminated SILEX funding.

In a May 1, 2003 press release, Michael Goldsworthy, chief executive officer of Silex Systems, said that his company disagreed with USEC's view of the potential and current state of the SILEX technology. “It is incomprehensible to us that USEC has decided to abandon the SILEX program only a few months short of completing the current test program and being in a good position to assess the economic performance of the SILEX process,” he said. As of July 2004, Silex Systems was still studying the economic feasibility of its laser uranium enrichment method.

It seems all laser programs with USEC left the building in the early 2000s so that Centrus could attempt to focus on gas centrifuges.

This started them on a long road to build a multi-billion dollar facility to enrich LEU via a small centrifugal plant in Piketon, Ohio. The DoE didn’t give them the $2b loan they needed to complete the project and the company proceeded to go bankrupt.

They restructured as Centrus Energy and began selling (or should I say reselling) LEU from Russia’s Rosatom to US and other western Utilities. This contract goes out until 2028 and currently is irrelevant until the US starts negotiations with Russia again (Centrus just got a nice little letter).

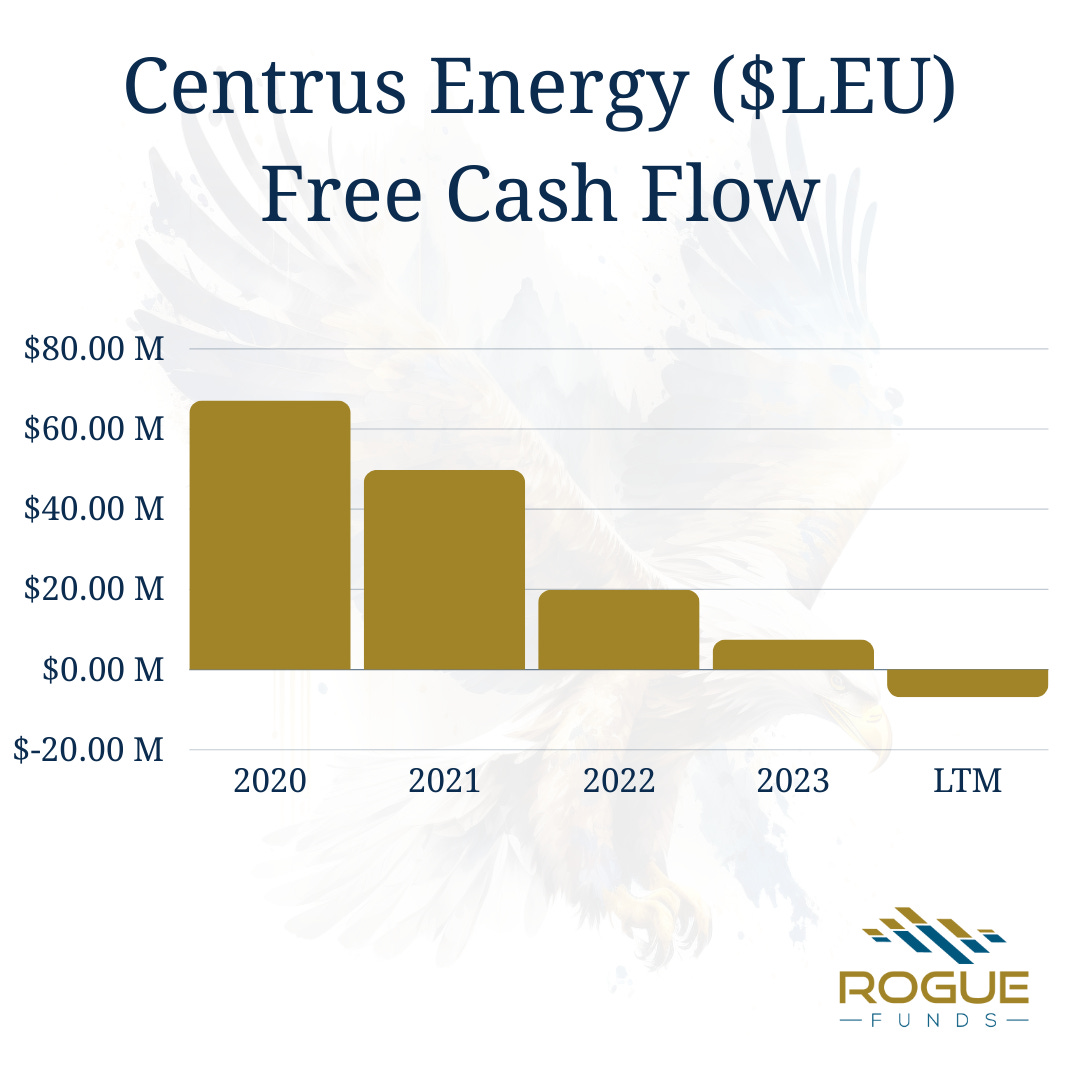

Even if this business stayed intact it doesn’t actually produce enough cash for them to fund a new facility to produce LEU or HALEU. In the last 6 years they have produced $150mm in FCF with every proceeding year since 2020 getting worse, and them actually producing -$6mm FCF in the last 12 months (see chart below):

To produce HALEU, Centrus has stated the following:

A full-scale HALEU cascade, consisting of 120 centrifuge machines, with a combined capacity to produce approximately 6,000 kilograms of HALEU per year (6 MTU/year), could be producing HALEU within 42 months after securing the necessary funding. With appropriate support, Centrus could add a second HALEU cascade six months later and subsequent cascades every two months after that.

This reads as 3.5 years for 6 MTU’s of uranium which hasn’t even begun yet. So we’ll assume this is a 2029-2030 target date (assuming they can start in mid-2025). The reality is they will need billions of dollars for serious amounts of HALEU, they have $200mm in cash and their entire business just went up in flames by Russia no longer sending Russian enriched uranium. Bank loans will be a nightmare to get (if it’s even possible) and essentially they will be relying 100% on the US government for their needed capital. Centrus is heavily incentivized to ensure that no foreign source of enriched HALEU enters the US, otherwise the DoE is no longer as incentivized to dump billions of dollars into their business. This can be seen in their constant US-only lobbying efforts.

PLEASE TAKE THIS TIME TO LIKE THIS POST

In 10 years there will be hundreds of MTUs (600+ per recent estimates) annually needed to fuel SMRs and in a best case scenario, assuming billions of dollars in government money (and assuming no delays like they are experiencing with their current 900kg HALEU plant), Centrus might be able to produce 100 MTU/yr by 2035 and that will cost them $4.5b in Capex to build out (about $1b per 1mm SWU). A lot of things have to go perfectly for Centrus in that situation and SMR producers are becoming very aware of this. If they find another solution, Centrus will lose any chance of a massive DoE contract.

SMR companies are waking up and beginning to find alternatives such as NanoNuclear taking a 5% stake in LIS Technologies and TerraPower signing a term agreement with ASP Isotopes. There is also strong evidence that Oklo might be the other SMR company that ASP Isotopes has signed an MOU with. As you can see, this is causing Centrus, who essentially has an MOU with every SMR company but no real path to actually producing enough HALEU for these companies, to have serious concerns in their ability to get funding from the DoE. If these SMRs find another source, the DoE will not feel pressure to supply an unprecedented large contract for a public company enricher. It seems like Centrus is selling hope (for a government contract) and are trading at $1.5b for their “business”.

Silex Systems

An Australian company that partnered with USEC in the 90s in an attempt to commercialize their technology. Silex was dropped by USEC along with the AVLIS program, as previously explained. CEO Michael Goldsworthy decided to stick with the technology and General Electric picked up the Silex licensing in the mid 2000s where their name was changed to Global Laser Enrichment (GLE). After giving them a facility in Wilmington, North Carolina they signed letters of intent with various US utilities. Once these were in place, GE spun off GLE and Cameco (the uranium company) also bought into GLE. The NRC then gave them licensing to enrich at the Wilmington facility in 2008. By 2012 they received a permit to build a commercial LEU facility.

By 2016, with still no commercialized production, GE decided to sell their stake in GLE and completely wrote-off the investment. In 2021, Silex took majority stake in GLE with Cameco owning 49% (with an option to move up to 75%). Their current plans show supposed commercialization by 2029 with LEU being the first target.

So what is going on with Silex?

Well, essentially Silex is a more advanced version of MLIS (explained from my initial article). Like MLIS it utilizes Uranium hexafluoride (UF6) which is a volatile gas and must be cooled to try to increase the amount of molecules in the ground state (almost no molecules are in the ground state without cooling). Temperatures have to be extremely cold otherwise you start getting “dimers” (isotope pairing). This extremely cold state is extremely unstable because any disturbance in the gas will cause it to crystallize. Feed gas is cooled by pushing the gas through a tube that rapidly expands, causing 95% of molecules to move into the ground state. This is where Silex and MLIS differ. MLIS technology then excites the vibrational energy of UF6 (U-235) with a CO2 laser which causes a chemical dissociation which creates UF5 and F which are then chemically separated via methane.

This is what we know of the Silex process:

MLIS and Silex have probably struggled due to dimer creation that occurs when UF6 is cooled. Also as we will see, Silex took an interest in higher laser repetition rates which can cause shockwaves (probably leading to crystallization issues). These repetition rates most likely lower the lifetime of instruments involved. This is probably their largest issue for selectivity and explains why they are targeting LEU over HALEU. The CEO has said they don’t plan on targeting HALEU until the mid-late 2030s and I am not convinced it’s even possible.

Due to their selectivity being about 2 to 20 (which is higher than MLIS and is most likely because they are targeting specific ions and not molecules as can be seen by the product/tail form), they are targeting LEU so they avoid having to go through multiple stages to get to HALEU as they are clearly expecting a large amount of issues in doing so. This is also why when utilizing depleted tails it is only to bring it from a depleted level to a natural level (which they must believe they can do in one stage).

When taking into account what Silex CEO Michael Goldworthy says, it should be noted that he has been singularly focused on commercializing Silex (nearly 30 years if they actually accomplish it in 2029). He has completely ignored the advancement of other technologies such as CRISLA. It should be noted Silex’s ex head laser physicist left to go be the CEO for the CRISLA technology (when Silex easily could’ve made a large investment/merged with the company years ago). I discuss CRISLA more in depth in the following section. I think he is ignoring the gains that have been made in the other nuclear enrichment fields and ignoring the significance of the scientists involved. It should be noted (as Paul has confirmed) Silex bought lasers from Klydon and needed their laser expertise (discussed later).

As you can see in the paper written above, ASPI’s predecessor (Klydon) provided both the lasers (confirmed by Paul Mann) and experts to Silex for their needs. Michael Goldsworthy probably isn’t super excited to talk about needing its now competitor for its own enriching needs. The paper then goes on to speculate on what Silex might be doing (and why their energy costs might be more than we realize), but this is complete speculation (the reason I am sharing the below photo even though it’s speculation is for future reference):

I am not sure if there is a lot of evidence they are using a stationary wall centrifuge but the Max Planck Institute Paper from 2015 has a lot more clout on this topic than I do.

LIS Technologies (Originally Called CRISLA, Inc)

LIS Technologies is a US based Laser Enrichment company that is championing their technology called CRISLA. The technology was invented by Jeff Eerkins who barely works with the company anymore. Christo Liebenberg (ex head of lasers at Silex) is now the CEO of LIS Technologies.

Let’s talk about Christo for a second… Mr. Liebenberg has an interesting history that we should explore. In the 1980s and 1990s Liebenberg worked with the South African government, working under Einar Ronander (this name should be extremely familiar to anyone who has researched ASPI, as he was the chairman of Klydon, owns stock in ASPI, and is one of the leading experts in the world in nuclear enrichment). While working in South Africa he actually can be seen on the 1999 PhD thesis of Mr. Hendrik Strydom (Chief Technology Officer of ASP Isotopes). See the below picture from Strydom’s PhD:

After becoming an expert in South Africa on Lasers he went and worked for Silex as their head of lasers for 5 years (2006-2011). Remember when I said we would discuss this later? Not only did Silex need experts from Klydon, they put them in charge of the entire laser program. His probable boss at Klydon is now the Chief Technology Officer of ASPI and co-author on some of his papers (Hendrik Strydom). South Africa (and ASPI specifically) most likely has the world leading experts on laser technology.

He then got an upgrade when he went and worked for ASML and helped develop their advanced high power, high repetition rate, CO2 MOPA laser systems used as the pulsed light source to generate EUV for photo-lithography. He has since partnered with Mr. Jeff Eerkins to commercialize CRISLA technology. Mr. Eerkins and Silex actually almost merged their companies:

CRISLA operates on a selectivity level less than Silex (roughly a selectivity factor of 2 which is not a whole lot better than centrifuges) but when exciting U-235 (via 5 µm lasers) they have two methods of getting the separation of the isotopes that they believe overcomes the issues of Silex and other MLIS strategies:

Free Jet Method: The gas shoots out a nozzle into a larger area and as it expands it gets colder due to the lower pressure forms pairs (dimers) between U-235 and U-238. As the jet stream continues the U-235 is hit by lasers and becomes excited, causing it to condense on the side of the cold walls and the U-238 continues in the jet stream until it gets caught in a streamer.

Cold-Wall Method: The gas flows past a cold wall, and the excited U-235 molecules, being the energetic ones, don't stick to the wall as much because they're too busy bouncing around, thus ending up more in the gas stream.

While this doesn’t sound super effective (because it isn’t) it is much easier to cascade stages in this environment since the product and feedstock are the exact same. This allows you to cascade the stages many times over for relatively low energy.

They are at a TRL-4 (Silex is at a TRL-6) and need around $500mm to commercialize the technology since CRISLA has never been tried at scale and the inventor of the technology, Jeff Eerkins, is near retirement. They think they can do it in roughly 7 years but with the NRC you never know how long it could take. I believe this could be the biggest threat to ASPI market share in 10+ years. They most likely won’t be an extremely serious threat in higher enriched isotopes or things such as HALEU or HEU due to the need for numerous stages.

Continued Response to Technical Concerns

Now that I have given context to some of their competitors, we can continue the breakdown of the short report.

Centrus chose not to buy ASPI

Centrus never offered or had the opportunity to outright buy ASPI according to Paul Mann (CEO). This was either offered to Klydon well before Paul and/or it never occurred. Either way I think it is safe to say that Centrus isn’t pro any laser technology and they definitely aren’t the best ran business on the planet.

Former Klydon Employee discusses Cameco Scientists

The former Klydon employee was so involved with the technology that they had no idea what the technology was, just what Cameco’s scientists thought of the technology? I don’t even know how to respond to this. Did Cameco try buying Klydon? Quantum Enrichment has only been in development for ~10 years and it wasn’t in extremely heavy development until they were purchased by ASPI, so are they talking about the Aerodynamic Separation Process (ASP) technology? That wouldn’t make any sense either because the ASP tech is universally accepted by enrichment scientists to work and it’s how South Africa enriched their nuclear weapon arsenal in the 80s. This isn’t exactly a hidden secret to anyone that it does work on uranium, so, they have to be talking about a very early version of quantum enrichment or the conversation never took place. This is another head scratcher.

In a further head scratcher, only two individuals who know Klydon/ASPI’s technology have left ASPI. According to Paul they both own stock in ASPI and they are both under NDA’s. Neither employee has ever been named. So this employee was clearly not someone of significance. Make of this situation what you will.

ASP has no Patents

This claim is digging up old news again (also brought up by JCapital months ago). First of all we know ASP technology works. Any enrichment physicist will tell you that ASP works (followed by a “but it takes a lot of energy”). There are no patents for ASP yet it obviously exists. When I talked to Paul about this I asked him if he would be willing to patent a laser if they invented a new laser and he said “yes”. The reason I asked him this because it is very clear they just don’t want to patent the process or anything that could give away their technological process. In their most recent press release (which was released right before the short report, on the same day) the filing reported that they did plan to patent some new pieces that they had invented in their ASP tech process for Silicon.

AVLIS Tech Failed Commercially because it is too expensive

This is where the short report ties the technology to AVLIS. In my original report I also made this connection by calling QE a modified version of AVLIS. Let’s dig deeper into the Lawrence Livermore Project that is being discussed here (also remember AVLIS, MLIS, and SILEX were all shut down by USEC/Centrus). We will utilize the exact source that the short report used to say why the plant failed and that AVLIS would fail:

However, the tests were interrupted by USEC’s decision in June 1999 to halt the development of the technology because a combination of near-term factors limited its funds. These factors included market-driven price declines for enriched uranium, significant cost increases to operate US gaseous diffusion plants, and the need to continue shareholder dividends.

USEC’s decision was no reflection on the advantages and capability of AVLIS. For example, AVLIS only uses 5% of the electricity consumed by existing gaseous diffusion plants, and AVLIS facilities would cost less to build than those for other enrichment technologies such as centrifuge technology.

[In reference to depleted tails] Revenue from enriched uranium produced by the plant, even at prices well below current market levels, would more than pay for both the plant’s construction costs and all operating costs. The market is currently at about $80-85 per SWU. Even at $60 per SWU, the DoE could recover all of its costs as well as generate a profit of $2.4 billion over the 25-year life of the AVLIS plant. This profit could then be used to more than offset costs to clean up the remaining 40% of tailings not economical for AVLIS enrichment. Hargrove says: “There’s obviously a lot of value in tailings that is waiting to be exploited.”

In the source that the short report used, it actually states that AVLIS was not a complete failure. The pilot plant alone had already processed thousands of kgs of Uranium and was able to sustain 400 hours of continuous operation without issues. It wasn’t until it moved to large commercial level that it began to have inconsistencies and issues which could have been solved but the project was cancelled due to cost overruns. This isn’t the only source that tells you the AVLIS tests weren’t a failure but until recently (specifically with the new need for HALEU) the nuclear fuel prices were not justifying the costs, along with every other R&D laser program in the world in the 90s.

The likely scenario is that unlike SILEX, who had a CEO who would die for its technology because it was only licensed to USEC, AVLIS was given to USEC and no one had the willingness to push ahead with it (pretty much every other global LIS program shut down within a couple years of the Lawrence Livermore plant) leading to its cancellation.

Why would no one want to explore this? Well essentially Russia’s flooding of the enrichment market along with the price of Uranium made it completely unviable to commercialize and compete.

It is a much different situation going forward thanks to the nuclear medicine field (which is finally beginning to take off) and HALEU. To put in perspective if we were to assume that AVLIS has not changed at all in 20 years (would be the only laser tech to not change at all) then the following paragraphs would explain this new value dynamic.

In 2002 the price per Separative Work Unit (SWU) was around $100/SWU for LEU with $60/SWU in AVLIS costs. This is $40/SWU in profits (already less than current HALEU profits) and required many more pounds of production for LEU.

Current market prices for enrichment for depleted tails to HALEU (.4% U-235 in South Africa) on a SWU basis is $155/SWU (assuming tails of .2% U-235 and product of 19.75% U-235) for 64 SWU to get from depleted tails to HALEU. ASPI obviously has access to South African depleted tails so they wouldn’t have to pay for feedstock or very little (which is roughly 50%-60% of the cost of HALEU) since they will be working with NESCA. From that article we believe Lawrence had $60/SWU for AVLIS (assuming zero improvements in technology in 20 years) meaning you would profit about $95/SWU and then you wouldn’t have to pay for depleted tails leaving you with around $18,920 gross profit per kg of HALEU processed utilizing the math below:

Estimation for HALEU revenue dedicated to the following which is roughly $10,000 for enrichment + $5,000 for Conversion + $15,000 feedstock = $30,000

$6,080 for enrichment costs ($95/SWU * 64 SWU) + $5,000 for conversion costs = $11,080 in HALEU costs

Gross Profit is $18,920 when assuming break even for conversion (which is extremely unrealistic when you look at prices of conversion). This is 63% gross margins assuming technology has not improved and SWU hasn’t improved.

Of course, a lot of their issues in the late 90s was due to the maintenance capex costs of AVLIS and they aren’t actually creating $20,000 per kg in FCF but it sure as hell makes the economics a lot more friendly, which seems to be the consensus of scientists at the Livermore plant as well. These cost/price dynamics are why companies like CRISLA and ASPI are now popping up.

The game changer for enrichers is HALEU and the companies with the least amount of Capex and lowest $/SWU will be the winners. AVLIS is notorious for being extremely low on initial capex since it’s fairly simplistic and low on $/SWU. It should be noted that for natural uranium to HALEU it’s about 45 SWU which is priced at $222/SWU. ASPI believes they have significantly improved on this process but even if they haven’t (there is a lot of evidence that they probably have and I will discuss later), they would most likely still be able to profit. Based on the tech claimed by the company, the bigger the enrichment the lower their $/SWU.

Now, why are medical isotopes also a game changer?

Getting a bit more technical… part of the reason HALEU is so hard to produce is because when you heat Uranium to 3400C it creates a lot of atoms that are in an excited state (meaning electrons are excited) which makes it harder to identify the individual valence band ionization energy with a laser. AVLIS only targets atoms in a grounded state which made their selectivity around 7 for uranium which is different for other elements.

For example in Hendrik Strydom’s (CTO for ASPI) PhD thesis, he experimentally used AVLIS to get a 112 selectivity factor for Lithium 6/7 (see below picture), most likely due to the less extreme environment and more ground state (not-excited) atoms and the fact that they processed the vapor very slowly. The good thing is that for elements like Ytterbium, roughly 95% of atoms when vaporized (probably somewhere around 700C-1000C) are in a ground state. The indication is that AVLIS would have a much higher selectivity factor for Ytterbium meaning less $/SWU than uranium making these other targeted elements much safer bets for AVLIS (if we assume they are using AVLIS, which I believe they are using something much more advanced).

In conclusion, the economics for both HALEU and medical isotopes are much friendlier to AVLIS now than they were 25 years ago if we assume no advances in technology.

Other Countries weren’t able to do it profitably

As stated above, essentially every government in the world was trying to use AVLIS in a time when you didn’t have the favorable economics of HALEU and or nuclear isotopes. All of those programs failed between 1990 and 2010. Also, what was up with highlighting Iran and Iraq like it’s something special that they couldn’t do it, I just thought that was funny.

The Picture on the IR Report hasn’t changed

This one also cracked me up a little bit. QE is clearly a more advanced and modified version of AVLIS (more on this later) but they way they ionize and separate is a similar concept. Who cares if they copied a picture on the IR presentation if it explains it well enough for non-expert investors. This one cracked me up and it definitely felt like a reach.

ASPI doesn’t have an NRC license

I don’t believe TENEX had a license with the NRC either. As ASPI has said before, the moment the product leaves their door it is the customer’s problem so they shouldn’t have an exporting issue involving the US if their customers possess all the required licenses.

Now to produce HALEU in South Africa they do need NNR licensing which comes as they build the plant (not before). At various parts of construction they will be granted NNR licensing. Obviously the scientists involved with ASPI and NESCA themselves will have experience working with NNR licensing and this doesn’t seem like a huge gateway in slowing things down. Dealing with the NNR should be better than dealing with the NRC. It should be something to pay attention to going forward.

If this “former centrus c-level executive” actually exists, he seems like a moron who barely understands HALEU regulations.

As far as this former Klydon employee (again, I am scratching my head on this), the response I would have to this is that laser enrichment is having a renaissance and we could make the same argument for LIS Technologies as well. It should also be noted ASPI is about to begin construction on their TerraPower HALEU site as shown by the MOU with NESCA.

Silex CEO Comments

As I brought up previously, Silex has an agenda in discussing its competitors (no different than if you talk to Centrus, LIS Technologies, and ASPI about each other). It should also be noted that Michael Goldsworthy has never really worked with an AVLIS facility or the technology that much. His low hopes comment seems to be irrelevant to the commentary here. Also other scientists at Lawrence Livermore seemed to believe otherwise per this source from the short report.

The cost is going to be way more than what ASPI is claiming

So first and foremost, ASPI isn’t trying to enrich in the United States where anyone who is familiar with the NRC knows that regulations are 75% of the cost when developing a new technology. ASP Isotopes already believe their technology works and should be proven via Ytterbium. According to Jeff Eerkins, the creator of CRISLA, if a country can enrich Ytterbium then it means they can enrich Uranium. ASPI believes they need about 12 x $5mm-$10 modular facilities/labs to run an SMR-scale throughput (so probably $80mm-$100mm for an SMR facility).

The expected cost for Centrus was going to be $2.5b for a 9mm SWU/annual facility (current centrifuge enrichment capex is about $1b per 1mm SWU/annually). ASPI isn’t building a 9mm SWU facility.

So why did Centrus not stick with AVLIS? It’s because of ballooning construction/maintenance costs (they experienced a $700m increase in expected cost from when they IPO’d to when they cancelled the project) and the fact that centrifuges had little risk to build.

The main reason that Centrus probably experienced this ballooning in costs is because when they got privatized they had to begin dealing with the NRC. When the AVLIS program was the DoE, the DoE did not have to go through the NRC for licensing. This was actually considered a risk by the Government Accountability Office when considering privatizing USEC in 1991 and discussing the AVLIS project. ASPI doesn’t have to deal with the NRC.

If we assume ASPI is just working with AVLIS (they aren’t) then it is very well known that initial capex costs are nowhere near as expensive as centrifuges (even with all of the cost increases it was still considerably cheaper). The former TerraPower employee has no idea what technology they have and of course the former Centrus executive would assume they’d need billions (because that’s what Centrus needs).

ASPI would be dumped by Russia if Trump creates a new deal

This is just ignorant. The expected NEI projections for HALEU demand in 2030 is 600 MTUs/annually (or 600,000 kgs of HALEU). Assuming that 1 kg of HALEU from natural grade uranium is 45 SWU then this would imply about 27 million SWU/annually will be needed in capacity. To put this in perspective, Russia only has 27m SWU annual capacity so they would need to double their current enrichment size to 54m SWU via ~$27b dollars in capex by 2035 (if they can even physically build that much capacity in 10 years). This is extremely unlikely to occur even if all of their focus flipped to HALEU. Russia cannot and will not be able to meet HALEU demand projections and SMR designers are very aware of this.

ASPI didn’t even bid for the newest contract

No laser company bid for the most recent HALEU contract. LIS Technologies, Silex, and ASP Isotopes have all said they plan on bidding for future contracts. The contract was not very large and you would be attached to providing the DoE with HALEU without a funded facility ($2.7b spread over 10 years and split among 4 companies and this is the maximum amount). It will be good to see them bid on future contracts.

Los Alamos Applied Physicist Says the Tech is Faulty

The short report has two parts dedicated to this physicist, so I decided to respond to it all in this section and it will be my finale in addressing every claim in the short report. I will follow this up by pointing out what the report missed completely. Before I dig in, Los Alamos has no history with AVLIS but they did work with MLIS.

This part highlights that we are not dealing with a nuclear enrichment expert by any means, not that I am one, it’s just obvious this person is not an expert in nuclear enrichment. Lets address his claims.

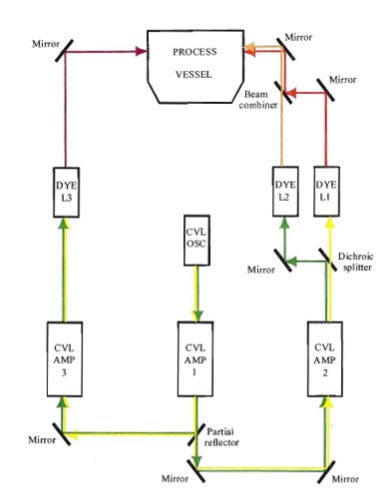

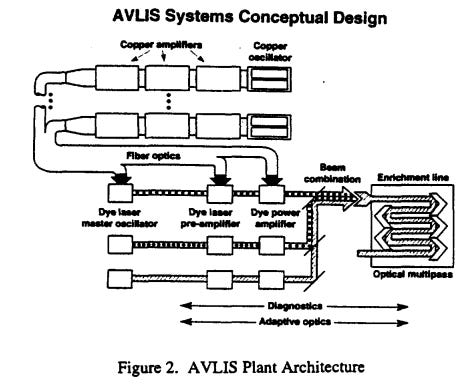

My first clue is when he said the high heat could damage the lasers. The uranium in Quantum Enrichment and AVLIS is heated up to 3400C and could damage certain parts, this is true and will be discussed later. The lasers are nowhere near the vessel where the vacuum and heated vapor travels through. If we look at Hendrik Strydom’s PhD paper he actually has a nice diagram of what AVLIS would look like and as you can see the lasers are nowhere near this Uranium vapor:

Let’s break down the image real quick. You have 6 lasers, 3 CVLs (Copper Vapor Lasers) and 3 Dye Lasers. As you can see on the labelled picture… none of them sit near the process vessel and instead sit in an ambient temperature environment (same with all mirrors). The lasers enter the process vessel via beam shaping and mirrors.

As we go into the Appendix of the report, this physicist proceeds to break down how this couldn’t work with one laser by referencing what I would consider the NRC’s “nuclear enrichment for dummies module”. This further explains that although this physicist is probably an intelligent individual (as shown by his understanding of evaluating the laser) it is highly, highly unlikely he is an expert in enrichment specifically.

The best part of this is that he says this is impossible with only one laser BUT if more than one laser and wavelength is used then the Dye Laser is accurate enough to only enrich U-235 and not U-238. In Hendrik Strydom’s paper where he uses AVLIS to enrich Lithium, he uses 3 dye lasers and 2 wavelengths (as can be seen in the picture above). So thanks to our short report author for proving that world renowned enrichment physicist, Hendrik Strydom, actually seems to know what he’s doing.

I believe I have responded to essentially the whole short report. Whatever claims were ignored will be discussed in the following sections. Most of the valid points brought up were brought up by the prior report, such as the Honig connection and Stenson connection. I believe the addresses for subsidiaries were also brought up in the prior short report. As for everything else? It doesn’t seem to hold water in my view and this was a very biased and cherry picked report. A lot of my response involved utilizing the same sources as the author (purposefully) to show how cherry picked his responses were.

PLEASE TAKE THIS TIME TO LIKE THIS POST

Laser Technology: What is Quantum Enrichment?

This whole response to the short report I decided not to defend ASPI by referencing their current tech, but merely responded by showing the impact if they were only using AVLIS. As you can see we aren’t up shits creek without a paddle if they were using AVLIS but lucky for us I do not believe they are utilizing AVLIS. This section will be fairly technical for investors with no scientific background.

Let’s talk about what Quantum Enrichment actually is and what the possible problems could be.

Quantum Enrichment (QE) is very similar to AVLIS. The largest difference between QE and AVLIS is that QE can identify and ionize atoms in a thermally excited state.

First let’s break down AVLIS:

The Uranium (or whatever element) is vaporized in a vacuum most likely via an electron gun within the process Vessel.

In AVLIS the next step is to excite the U-235 atoms. This is done by pumping/amplifying the dye laser with a solid state laser (older techniques utilized copper vapor lasers, such as at the Lawrence Livermore project). The wave lengths of the laser could only be absorbed by ground-state U-235 atoms as the wave lengths of excited atoms create a doppler broadening effect that changes the wave frequency and makes it impossible to efficiently ionize.

The next step is a second dye laser (also pumped via a solid state laser) further excites the atom, further improving selectivity and prepping the U-235 for final ionization.

A third laser (pumped via a solid state laser) ionizes the selectively excited U-235 atoms based on the desired wavelength they have after absorbing photons from the first two laser rounds. These atoms are now ready for separation.

The ionized atoms are then separated when an electric field is applied to the vapor stream and moved to a collection vessel.

AVLIS would experience a selectivity of 7 which is high but not great because it was only able to target U-235 atoms that were in the ground state (roughly 40% of atoms). Also due to the focus on LEU the scientists most likely sped up the vapor stream to ensure the selectivity was not too high. I believe a selectivity of 7 for uranium with AVLIS is misleading because if you slowed the vapor down you would be able get an extremely high selectivity. This slow vapor stream could be seen with Lithium in Strydom’s thesis when he got a selectivity of 112.

In the 1990s at Lawrence Livermore they would also get this “non-selective vapor build-up” that would impact the vessel which is where I believe they experienced corrosion (also possibly on the collection vessels that most likely contained copper to attract the ions). This non-selective build-up might have impacted selectivity as well.

Strydom partially solved for this via shutter plates in his PhD thesis and by the mid 2000s a study was done that showed .1% build up when working with Lithium. Lawrence Livermore scientists consider their AVLIS program a success and funding/uranium enrichment industry dynamics are the main reason it probably isn’t in use today.

What is Quantum Enrichment (for Uranium)?

What we know:

The Uranium is vaporized in a vacuum most likely via an electron gun within the process Vessel.

Lasers excite both ground-state AND thermally excited U-235 atoms. How this is done exactly is unknown, but it definitely involves a significant amount of laser beams (well more than 3).

Quantum Enrichment involves much more advanced spectroscopy (this could or could not include the following: pulse shaping, beam shaping, adaptive feedback control, pulse sequencing, etc.).

The second laser step probably involves further excitement to the already excited U-235. This also probably involves multiple lasers exciting specific U-235.

By targeting both excited and ground-state atoms, the selectivity is much higher, near 678 for Uranium.

In the last laser step it will take all of the excited U-235 atoms and ionize them.

The ionized atoms are then separated when an electric field is applied to the vapor stream and moved to a collection vessel.

Due to the high selectivity the temperature and vapor speed has to be variable and controlled to ensure that some non-selective buildup sneaks into the product otherwise they would have nuclear proliferation violations by enriching well beyond 19.75% (the limit for HALEU) by accident.

Near 100% of feedstock ends up in the tails or product (which lines up with previous studies I saw). The remaining is cleaned up with Nitric Oxide as needed. I believe this might be where their corrosion issue has been solved.

That is what we know (which isn’t much but it gives us a pretty decent picture).

I will now take a stab at what I believe they are doing. Remember this is where things get very fuzzy/speculative and relies on a lot of guess work. Again, I am not a nuclear physicist but I will take my best shot at it for fun. This section should be taken with a grain of salt. Even if I was a nuclear physicist, there is a large difference between being a laser enrichment expert and a nuclear physicist.

What I think is occurring?

Why are excited atoms so hard to energize properly? The reason is because when they become excited their valence band wavelengths undergo a Doppler Effect which causes their wavelength to overlap with the wavelengths of excited U-238. This is called a Doppler Broadening Line. The proper wavelength is needed for the valence band to be energized.

EDIT: I changed valence band energies to valence band wavelength and added more info about absorption.

To overcome this I believe QE is utilizing many lasers to excite both ground-state AND thermally excited U-235 atoms to cover all wave lengths within this Doppler Broadening (40% of Uranium atoms are in ground state, 30% are in a slightly excited state, and another 30% are in an extremely excited state). But wouldn’t this be energizing U-238 along with U-235? My answer is that they are most likely utilizing pulse shaping (I believe pulse shaping is the most important part), beam shaping, pulse sequencing, and/or possibly adaptive feedback control to ensure that the photons can only be absorbed by U-235 while ignoring U-238. (This has NOT been confirmed by the company or Paul Mann)

I believe they then continue to step up the energization/excitation of U-235 to ensure high selectivity, except they have to utilize numerous lasers and spectrometry to ensure that all of these isotopes are getting hit again. This probably involves multiple steps of lasers.

They do this until the lowest energy U-235 atoms have been stepped up and ionized.

Obviously this is probably wrong in some respects but broad enough to cover most of the process for our purposes. There is really no need to speculate on what exactly they do because we are not experts in laser enrichment.

For other elements such as Ytterbium-176 and Lithium-6/7, a lot of these atoms do not leave the ground state when vaporized (95% of atoms do not leave the ground state for Ytterbium and 99% for Lithium). This means that the more complex spectrometry is not needed to ensure high selectivity and this most likely means it a very similar process to AVLIS (meaning much lower risk of success). They will still probably want to test out the Quantum Enrichment technology to ensure it works on excited atoms through Ytterbium and it will be a decent test of the technology. As Jeff Eerkins says, if you can enrich Ytterbium then you can enrich Uranium.

The importance of this high selectivity means they make serious efficiency gains as you go to a higher enrichment of U-235. For example, if they received a HEU contract with the UK (or US) Navy then their $/SWU would scale immensely. It also scales immensely when utilizing depleted tails for the same reason. This selectivity means they also don’t have to worry about cascading stages which is huge for commercialization purposes. Another great part about this high selectivity is that you don’t need to process as much uranium which means less maintenance.

Why do I trust that this information is correct?

Well, as we have already seen, Mr. Strydom is an expert in laser enrichment and he even invented the ASP process. Ronander is one of the most cited individuals in his field.

One of their coworkers, Liebenberg, (who worked under Ronander) worked as the head of lasers for Silex and as a laser physicist with ASML, he is now the CEO of LIS technologies. LIS Technologies is one of TWO other laser enrichment companies in the world. Silex hired Klydon scientists and bought lasers from them. That essentially makes South African experts involved in the only three laser enrichment companies in the world. Strydom and Ronander are the best of the best when it comes to experts in the field.

A good friend of mine has seen the facilities along with 20 other investors.

Lawrence Livermore scientists believe their AVLIS project was a success but was just cut due to poor industry dynamics. It seems in the last 20 years since the Lawrence Livermore project, AVLIS experts had already figured out a lot of the corrosion issues by reducing selective build-up. Recent studies for Lithium said they had reduced build up to below .1% and Paul Mann said this remaining build-up was easy to clean up.

The good thing about commercialization of this AVLIS process is that the company does not plan to build extremely large facilities and they want to keep everything at a roughly “lab” size. This means having smaller, modular set-ups, that does not require creating commercial sized set-ups. This could reduce the commercialization risk significantly.

Even if the complex spectrometry does not workout for commercializing HALEU (which doesn’t seem to be the case), they can easily fall back on the simpler elements that AVLIS is proven to work on due to a high percentage of vaporized ground state atoms (Ytterbium, Lithium, etc). This is still an extremely large market on its own. They have no/little capital at risk as TerraPower is expected to fund most of the HALEU facility.

The Forgotten Technology: Aerodynamic Separation Process

A huge thing missing from this report is the Aerodynamic Separation Process technology. This is the other half of ASPI’s business and it’s not discussed at all. The most likely reason for this lack of acknowledgement is that no one disputes this technology in any capacity. Nuclear Medicine and Silicon will be the only parts of the business that will be producing revenue and cash flow over the next 2-3 years and a lot of that will flow through ASP technology.

The biggest issue with ASP technology is that it is extremely energy intensive (although less initial capex since it is a stationary wall centrifuge). This is addressed via the company’s move to Iceland where they will receive energy prices for 1/5 to 1/7 their current energy prices. This will allow them to compete on energy prices as well as much lower capex than gas centrifuge. This will create a strong competitive advantage when competing with other enrichers.

This is how I explained it in my original article:

The Aerodynamic Separation Process, aerodynamically separates the molecule via a stationary wall centrifuge paired with proprietary flow directors to separate isotopes of varying levels of atomic mass. Similar to a gas centrifuge but without needing to move the centrifuge or have nearly as many stages. I would describe it as similar to rifling in a gun barrel that the molecules (usually gas) are sent through at high velocity. It is a much more efficient capex process than Gas centrifuge basically due to less moving parts.

More detailed technology review can be found at this study: https://klydon.co.za/images/asp_2012.pdf

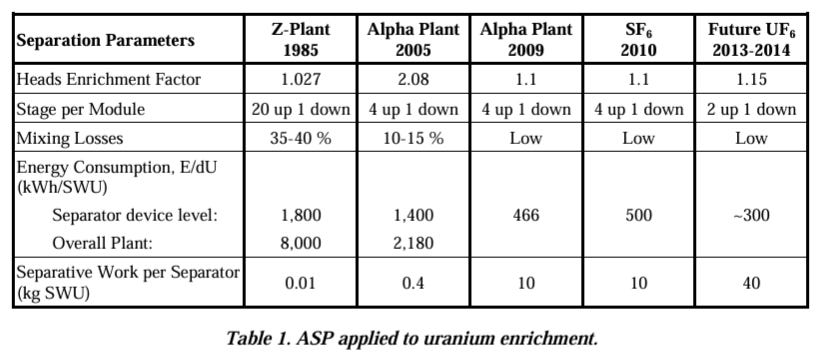

What is the selectivity factor and kwH/SWU

Within the study in the above quote, the following selectivity factor (1.15 which is on par with gas centrifuges) for UF6 is shown along with the following kWh/SWU (~300). Obviously they have a long way to compete with the 50 kWh/SWU of a modern gas centrifuge but also this data was from 10+ years ago.

According to Paul they have experienced better efficiency gains and I believe they most likely sit below 150 kWh/SWU for their first Iceland plant, by using hydrogen as a carrier gas over helium. I am not sure what their first Silicon plant in South Africa will be in terms of cost because they couldn’t use hydrogen since the plant is in a crowded area where a highly combustible gas like hydrogen isn’t advised.

This is not cheap in terms of $/SWU. By moving to Iceland their average cost ($0.05/kWh) is roughly 1/5 the cost of the average US price ($0.25/kWh) and 1/2 the lowest cost in the US ($0.10/kWh). This makes it much more likely they will be able to seriously compete on all of these light gases (most gas centrifuges can’t do light gases anyways, they need something with more mass).

The Separative Work per Separator should be read as initial capital expenditures. The more they can process in one separator, the cheaper their initial capex outlays. This allows them to rapidly and cheaply build out large production capacity which gas centrifuges cannot do. What might cost ASPI 10+ million dollars in initial capex might cost a gas centrifuge operator hundreds of millions.

The opportunity in Nuclear Medicine

The opportunity in Nuclear Medicine is huge and I explained it in depth in my original article which I highly suggest you check out.

PET Labs

Pet Labs introduces a very unique opportunity for the company to vertically integrate that business and create competitive advantages against competition. If they can build out a large cyclotron base then that will allow the business to grow. If the company is able to get FDA approval for cyclotrons for things such as Mo-99 then this could eventually become a decent part of the business. It is too hard to speculate on the impact of this business in the future.

The opportunity in Silicon-28

Currently I only know of two other sources that can produce pure Silicon-28, Silex and Rosatom. Rosatom can only enrich silicone tetrafluoride and Silex can only enrich halo-silane. Both of these companies require chemical conversion to the silane form after enrichment which most likely introduced some impurities into the silicon (this silicon is enriched to 99.995%+ for quantum computing needs and purity is extremely important). This is where ASP’s ability to work with light gases comes into play because they can directly enrich the usable form of silicon, Silane (SiH4), without converting it.

The facility in South Africa was officially constructed at 5x the size of the expected facility size and will be able to process over 50 kgs of silicon. We know the company already has MOU’s for at least 10kgs of its silicon production and we should start seeing a lot of interest continue. I think as far as I have researched, they have the largest pure silicon enrichment plant in the world. Now that the plant is completed this should bring revenue in Q1 of 2024 and the expansion of the plant most likely led to the delay in the Silicon-28 plant.

How big is the quantum computing opportunity in Silicon-28?

First, there is quantum computing which is huge. All silicon wafers for quantum computing will have to be made via pure silicon. The quantum computer chip market is roughly $150mm right now and growing at 43% per year. They will most likely get a sizeable revenue chunk of this since every wafer will have to be pure Silicon-28. Also, now with them producing so much I believe we will see more studies come out on Silicon-28 for both quantum computing chips and commercial semi-conductors. There has never been easy access to Silicon-28 and there could be advantages found that we did not know of. The ease of access to pure Silicon-28 could also solve a bottle neck for the quantum computing industry and release much higher growth. Quantum computing could also explode in growth as Moore’s Law hits a wall (the best transistors are only ~20 silicon atoms across).

How big is the opportunity in advanced semi-conductors?

It was recently found that Silicon-28 semi-conductor nano-wires are able to conduct heat nearly 150% more efficiently. This is because the phonons in the wire don’t get stuck in the impurities from Silicon-29 an Silicon-30, allowing for the wire to easily move the phonons and disperse the heat. This effect seems to get more pronounced the smaller transistors/nano-wires get. The smaller this gets the more impurities will be an issue. It also seems to bode well that instead of getting smaller, stacking is going to be the future of the semi-conductor industry (meaning more nano-wires). This will allow computing to scale.

Let’s do some math to see what the opportunity is just for Nvidia blackwell chips for example. I am not a chip expert and this is a SWAG (scientific wild ass guess):

A wafer can make about 60 Nvidia dies (edited). Wafers are fairly universal sizes.

.775 mm is the usual thickness of a wafer with a universal 300mm in diameter

This is an area of 70685mm^2 (edited)

Volume is 54,780 mm^3

54,780 mm^3 * .0023 g/mm^3 (density of silicon) = 126g per wafer

This would mean 2.1g per die (126g/60 dies). This does not accommodate for die yield which is not readily available.

Let’s assume nano-wires are 1/20 (5%) of all of the silicon involved in a die which would be 0.105g of pure silicon needed (complete guess but seems very conservative based on my research on gate all around transistors which the nano-wires/sheets will be used with).

SMC, Samsung and Intel have all announced they will be using this design in the coming years. This list would most likely include one of ASPI’s customers for silicon.

If you read the article you will see there is a very high chance it is much more than 5% of the transistor will be nano-wires, but I like to be conservative.

Nvidia uses 2 die per Blackwell GPU which means that a possible .21g is dedicated to the nanowires.

Nvidia is expected to sell 3,000,000 Blackwell GPUs in 2025.

This would imply $315mm for nanowires from just Nvidia and roughly 630 kgs of pure Silicon-28. We were also conservative because we did not accommodate for die yield.

$500k per kg of Silicon * .21g of pure Si-28 per GPU * 3,000,000 GPUs = $315mm

If ASP Isotopes is able to get the price of Silicon down to $20/g as they claim, then we could begin to see entire wafers get built from pure silicon and their TAM would explode as it would be able to be used in almost any application at that price. Based on my research into quantum computing chips I believe one of the semi-conductor companies they have a purchase order from is Intel which means they will also be testing commercial applications of Si-28. It will be interesting to see what studies come out as commercial semi-conductor fabs get ahold of this pure Silicon. It is also extremely likely that if the large fabs really like the efficiencies from pure Silicon-28 they would probably help fund large capex plants in Iceland (similar to TerraPower and the HALEU facility).

I think it is very easy to see where a ton of value could be squeezed out of the ASP technology and I don’t think it was accidental that it wasn’t discussed. I see this technology as extremely de-risked and I think most other enrichment physicists would believe this as well. The TAM for Silicon alone is in the $10+ billion dollar range.

The True Risks

The short report highlighted some risks but here I will highlight what I consider to be the true risks or risks that I know many investors are worried about. I have since adjusted the risks I found since my last write-up on the company.

Quantum Enrichment Commercial Risks

This risk is very real but I believe it is not as high as people believe. First and foremost the process is similar to AVLIS except with 20 years’ worth of additional knowledge and new tech (and the Lawrence Livermore project was considered a success by those involved).

A question one also has to ask is why would these laser enrichment experts decide to release and commercialize a new technology in their 60s/70s when they could’ve done this at any point in the last 20-30 years? Clearly something has occurred with the technology that they feel very comfortable with or the economics have changed in their favor.

PLEASE TAKE THIS TIME TO LIKE THIS POST

The biggest risk will be what makes this “Quantum Enrichment” which is the ability to selectively ionize atoms while in a thermally excited state. This could have issues as it scales since it has not been done on Uranium before. I believe the modular and more lab based facility designs will help in de-risking the commercialization process.

I believe the risks to Ytterbium and Lithium are extremely low along with other elements that stay in a grounded state during vaporization. But they could be good tests to utilize for Uranium. I assume these tests have already been proven and it’s why a month later TerraPower released the Term Sheet Agreement.

Delays in Product/Revenue/FCF

A big issue with the company has been delays in the realization of revenue. This first came in the form of a contract for Mo-99 and Mo-100. They realized a small (non-refundable deposit) from a US based client and a contract with BRICEM (chinese tech institute). According to Paul neither client was ready to receive Mo-100 and that is why the company turned its second ASP plant to Silicon-28.

The second delay came from Carbon-14 which has been continuously delayed and many investors began to believe there was smoke and mirrors here. I decided to reach out to the CEO of RC-14 (their customer for Carbon-14) and asked him a few questions. This is his response below:

Q. My understanding is that you were working with a Tennessee company and it (carbon-14) got stuck there or they lost their license to handle it (I could have this wrong). I am a little confused on how the shipping works and what exactly occurred to cause this year+ delay, can you explain this a bit more in depth? Why was it in Tennessee at all? Why did it get stuck there?

A. Yes a portion of our inventory is stuck in Tennessee where we harvest the Carbon-14. We haven’t ship yet the C14 because we need to process more inventory to make the first shipment. We experienced some unforeseen delays in our process, which have delayed the production of low-concentration Carbon-14.

Q. Are you currently processing more feedstock? Do you have to go through this Tennessee process again?

A. The production is planned to restart in January and yes the production happen in Tennessee in a licensed facility.

Q. When are you hoping to get the C-14 processed and shipped?

A. Q1 2025

Q. When do you hope to have the C-14 delivered to ASP Isotopes?

A. We plan to ship low-concentrated C14 to ASPI by the end of the Q1 2025.

Q. What exactly is your process of getting this slightly enriched Carbon-14 from a nuclear reactor (natural carbon-14 is in the trillionths of percent)? You don't have to answer this but it's more just my curiosity.

A. The C14 is extracted (harvested) from a nuclear waste generated by CANDU reactors in Canada. Our technology allows to remove the C14 out of the waste which will ease the long-term storage for the nuclear stations. Once the C14 is isolated, we have developed a process to valorize the C14 and one of the steps in our process includes ASPI technology to enrich the C14.

As you can see from the CEO of RC-14, this delay is not on ASP Isotopes at all and rests on delays with RC-14 (obviously not great but clearly Paul was not lying to investors). This would also mean that supposedly we’ll get revenue in Q1 or Q2 barring the RC-14 doesn’t get delayed again, and we should recognize more than $2.5mm. I believe there was a licensing issue with the Tennessee facility that has been resolved.

The third delay came from Silicon-28 which was supposed to start producing revenue this quarter but clearly it was delayed to expand the facility significantly (5x original guidance). Since construction is completed and commissioning doesn’t take as long for ASP plants, I expect revenue to begin being recognized in Q1 of 2025 for Silicon.

Ytterbium-176 wasn’t supposed to be completed until next year and commissioning was estimated to be 3-6 months beyond that. That would put the original guidance around early 2026 for revenue from Ytterbium. Currently they plan on sending out samples in Q1 of 2025 and if we’re lucky they will experience revenue in Q1 2025 as well. I think there is a high likelihood that revenue is not recognized until Q2 2025.

The TerraPower contract will be recognized in part this quarter.

Unrealized Demand from SMRs

There is a huge risk that SMRs don’t pan out like we expect them to and demand is much less than anticipated. There is an even higher likelihood that they are delayed. The good thing is there isn’t a lot of capital being lost here as TerraPower plans to fund most or some of this facility. I think Elon Musk (unironically) could help clear out some of the regulations along with motivation from Congress seen in recent years (such as the Advance Act). This helps de-risk this slightly. The good thing is that it seems TerraPower (the furthest along SMR) has developed a close relationship with ASPI.

A lot of this risk is completely outside of ASPI’s control and why the business should be looked at for every part of its business, not just nuclear.

Unrealized Demand from Commercial Semi-Conductor Fabs

There seems to be very little risk with quantum computing fabs. They NEED pure silicon-28 and it’s hard for me to imagine the risk involved there. The main risk regarding QC specifically would be if they found another usable material.

Now with the commercial semi-conductor fabs we are relying on the nano-wire study heavily and the customers finding out new use-cases for pure Silicon-28. Since they already have two purchase orders in place, there is a very high likelihood there are use cases that we do not know about it. Especially since one of the companies is an industrial gas company (I have no idea what that use case is). Based off of the expansion to 50 kgs, this implies this risk is not extremely elevated as it most likely means there is very strong demand for pure Silicon-28.

Conclusion

I believe I have addressed most points in the short report and expanded on the risks not highlighted in the report. ASPI has many shots on goal and I believe they will be able to deliver on most if not all projects.

I believe most ASP tech isotopes are extremely de-risked as this technology has been proven. ASPI most likely has the worlds leading experts on laser enrichment. The question you have to ask yourself is why would Klydon executives all of a sudden make these claims regarding laser enrichment when they know the risks of AVLIS and scaling. It feels safe to say that they have clearly found something in their past 10 years of research that has led to Quantum Enrichment. Don’t forget the tech has already been proven to enrich Ytterbium-176.

Having two purchase orders, one of which is a large semi-conductor company (which I believe to be Intel) shows extreme interest in their second non-QE element, Silicon-28. I also assume extreme interest contributed to massively expanding the original plan for the Silicon plant. We also have low risks in isotopes that will provide further revenue in their medical isotope business for things like Molybdenum, Nickel, Zinc, and Xenon. This isotope list will probably be expanding due to the broad use cases of their technology.

Overall I feel that there are various aspects that de-risked the technology risk and most delays in Revenue/FCF can be explained. The TAM’s are huge and they will have temporary monopolies (if not permanent monopolies) in almost every isotope. I think Paul is right in delaying revenue to expand these plants as it provides much more efficiency (and it makes sense for his comp plan as explained in my previous article).

The company will be seen as borderline completely de-risked upon revenue recognition from Silicon-28 and Ytterbium-176 which would also create positive free cash flow. I believe we should expect revenues of $40mm+ in 2025 and over $100mm in 2026. They have a Zinc and Xenon facility coming online in 2025 and I expect a Silicon Iceland facility to be discussed in 2026 along with Nickel and Lithium. The sky is the limit for this company and we believe 2025 will be a huge year for the company.

We have not sold any shares since the short report and we are long ASP Isotopes.

Disclaimer: The author of this idea and his Fund have a position in securities discussed at the time of posting and may trade in and out of this position without informing the reader.

Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

This article may contain certain opinions and “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential,” “outlook,” “forecast,” “plan” and other similar terms. All such opinions and forward-looking statements are conditional and are subject to various factors, including, without limitation, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors, any or all of which could cause actual results to differ materially from projected results.

As a generalist who has no deep insight into the technology, I got totally scared by the short report and sold out. Easy for me to do, as I was sitting on a big profit. After reading some chatter on X and your report now, I may as well come back at a lower cost.

I have to say I have great respect for the depth of your top notch research!

thanks, I really appreciate you taking the time and effort to share you hard work with the public thanks and good luck.