New Study Release is Giving Achieve an Incredible IRR

(Please review the disclaimer at the bottom of the post)

Achieve Live Sciences is giving an incredible IRR at the current moment after their substantial news release from January 7th (which can be view here). The news release has the following highlights:

Over 300 Participants Have Completed Cumulative Six Months of Cytisinicline Treatment in the ORCA-OL Trial, Completing the Long-Term Exposure Requirement for NDA Submission

ORCA-OL Long-Term Exposure Timelines Remain on Track with No Safety Concerns Identified

Planned Cytisinicline NDA Submission on Target for Q2 2025

PLEASE TAKE THIS TIME TO LIKE THIS POST

This is huge, as it allows them to submit their NDA in April/May and they are on track with zero safety concerns in this first half of the trial. As the drug has breakthrough designation the odds of a priority review is extremely high (especially with it's efficacy and high tolerance compared to the previous category leader... Chantix, which is now generic). The risk/reward ratio has become extremely skewed as ACHV sits near 52 week lows while it is extremely de-risked and could become a multi-bagger before years end.

I have previously written up a recent article on Achieve ( ACHV 0.00%↑ ) which can be found below:

I'll summarize the opportunity here:

Achieve is utilizing a nicotine cessation drug called Cytisinicline, which has showed success over multiple phase 3 studies.

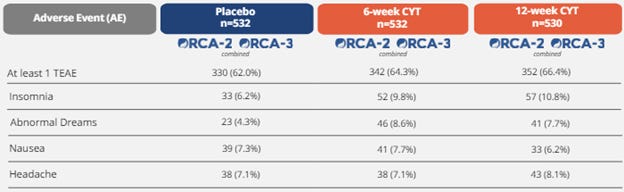

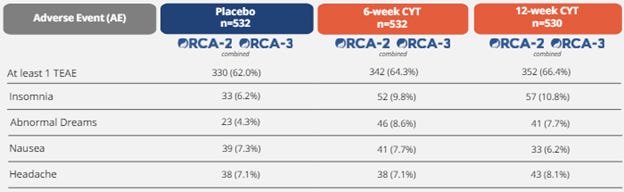

FDA requested long term safety studies (300 patients for 6 month study and 100 patients for 12 month study). 300 patient study was completed with no safety concerns. Of those 300 patients, another 100 patients will use the drug for another 6 months (June/July timeframe).

FDA said they could submit NDA after the 300 patient, 6 month study. They said the one year safety study could be submitted after NDA approval (essentially showing that they will just make a label change if one year results come back poorly). Shouldn't impact drug approval in my opinion.

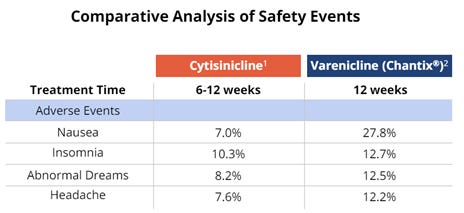

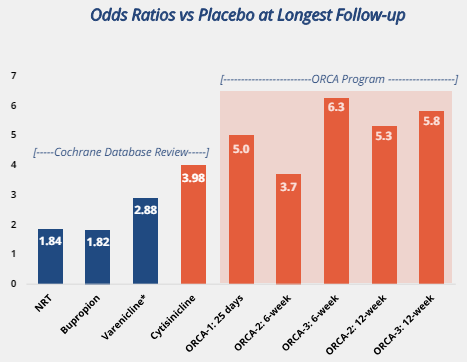

The odds ratio (or the multiple of success vs placebo) for Chantix was 2.88 for a 12 week trial (meaning you had a 2.88 times better chance of abstinence vs placebo). For comparison, Cytisinicline has an odds ratio of 3.7 for its 6 week trial and odds ratios of 5.0-6.3 for its 12 week trials.

It's results also showed significantly less side effects when compared to Chantix.

It’s side effects profile was extremely similar to the normal side effects felt by nicotine withdrawal:

The current generic drug course runs about $475 and Cytisinicline could probably push a much higher price probably close to $700-$800 based on how Pfizer was able to sell Chantix. If we assume a 30% market share (which isn’t as high as I think it will go) which would be about $300m in revenue per year and this implies a valuation of ~$1B (just over 3x sales). With a 60% market share this would imply $600m in revenue and a 1.8B valuation at 3x sales.

When accommodating for 55m shares diluted, this leaves the company with a very conservative valuation of ~5x-10x their current valuation ($15/s-$30/s).

Based on their new investment banking board members and only raising enough cash to Q3 2025, I believe there is a high chance of a buyout in 2025.

With the 6 month trial out of the way, I believe there is a serious de-risk to the company as we now see a better view of the long term impacts (along with the fact that this is licensed in Europe with no major side effects). By July of this year we should get the 1 year results with a run-up happening at any point.

If they receive priority review (which I believe they will with their breakthrough drug designation and incredible efficacy/safety compared to Chantix) then we could see PDUFA by October-December of this year. This would push their IRR significantly higher.

I believe NDA approval will catch the attention of biopharma catalyst funds to start driving up the price when they see the obvious mismatch in value.

I highly suggest checking out my previous blog post (linked below) for a full picture. Currently the price is at 52 week lows while it is the most de-risked it as ever been.

Disclaimer: The author of this idea and his Fund have a position in securities discussed at the time of posting and may trade in and out of this position without informing the reader.

Opinions expressed herein by the author are not an investment recommendation and are not meant to be relied upon in investment decisions. The author is not acting in an investment adviser capacity. This is not an investment research report. The author's opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is illustrative in nature, limited in scope, based on an incomplete set of information, and has limitations to its accuracy. The author recommends that potential and existing investors conduct thorough investment research of their own, including detailed review of the companies' SEC and CSA filings, and consult a qualified investment adviser. The information upon which this material is based was obtained from sources believed to be reliable, but has not been independently verified. Therefore, the author cannot guarantee its accuracy. Any opinions or estimates constitute the author's best judgment as of the date of publication and are subject to change without notice. The author and funds the author advises may buy or sell shares without any further notice.

This article may contain certain opinions and “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential,” “outlook,” “forecast,” “plan” and other similar terms. All such opinions and forward-looking statements are conditional and are subject to various factors, including, without limitation, general and local economic conditions, changing levels of competition within certain industries and markets, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors, any or all of which could cause actual results to differ materially from projected results.

Is the report from STAT news the latest: ACHV CEO expects FDA approval mid-2026

https://www.statnews.com/2025/04/30/new-stop-smoking-drug-achieve-life-sciences-seeks-fda-approval-for-chantix-competitor/

Interesting! I believe you have a logical argument in this article. What are your thoughts on any risks involved in completing the final phase of the trials, specifically the data from 100 patients over a year? Do you foresee any risks?